Seamless one-tap transactions, AI-powered insights, instant payments, and deeply personalized financial tools have collectively shifted what customers expect from their bank – across every region, income bracket, and generation. To navigate this new global reality, we have compiled the most up-to-date mobile banking industry statistics drawn from worldwide market data.

Key statistics on mobile banking

- The mobile banking market will grow from $1.87 trillion in 2025 to $6.42 trillion by 2033.

- There are 2.3 billion registered mobile banking accounts globally, with 593 million active monthly.

- 42% of consumers now prefer mobile apps as their primary way to manage finances.

- 84% of users are satisfied with their current mobile banking experience.

- GenAI could unlock $95.6 billion in value across banking functions.

- 72% of banks cite data quality issues as a major barrier to AI adoption.

- 82% of financial institutions now operate in hybrid or multi-cloud environments.

- Cloud adoption cuts banking IT costs by up to 30%, saving institutions up to $2.4 billion annually.

- 50% of banking executives expect VR/AR to eventually break through, signaling long-term conviction despite short-term caution.

- Super apps achieve up to 80% customer retention, compared with 50% for traditional banking apps.

Mobile banking market statistics

Banking is moving away from standalone financial products toward integrated experiences that fit naturally into how people live, spend, and plan. The statistics below capture the scale of that transition: where adoption is accelerating and where the biggest structural changes are taking place.

The global mobile banking market is set to more than triple in size

The global mobile banking market is entering a high-growth phase, projected to expand from $1.87 trillion in 2025 to $6.42 trillion by 2033, at a 16.8% CAGR. This sharp acceleration signals a structural shift toward mobile-first financial services, driven by digital adoption, real-time payments, and increasing reliance on smartphones as the primary banking channel.

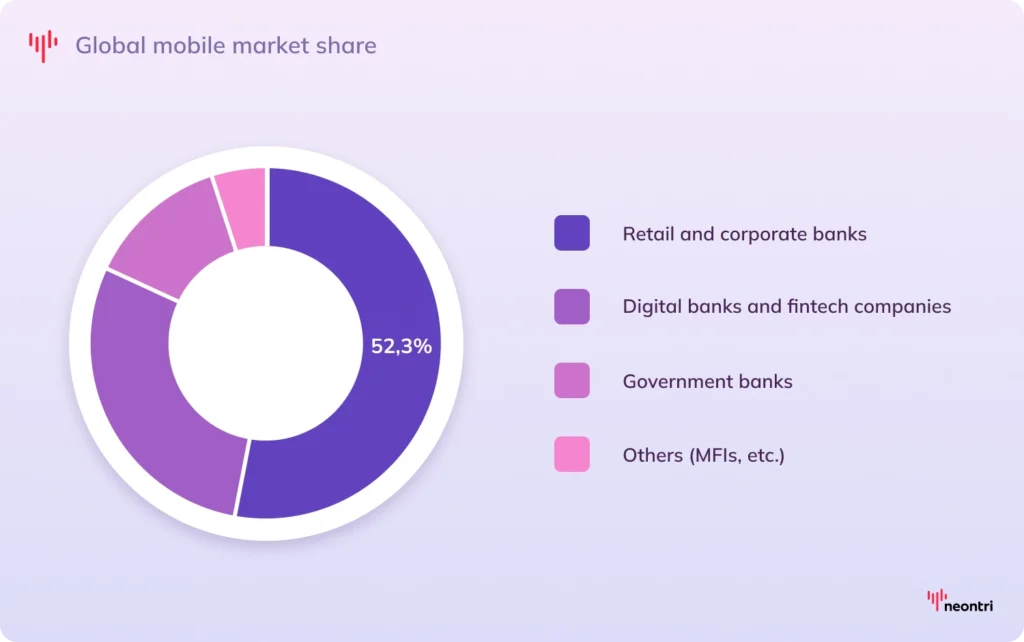

Retail and corporate banks hold over 50% of the mobile banking market

The global mobile banking industry spans retail and corporate banks, digital banks and fintech companies, government banks, microfinance institutions and other financial service providers. Among these, retail and corporate banks dominate with a 52.3% market share, driven by their large customer bases, established trust, and continued investment in mobile platforms.

There are 2.3 billion mobile banking accounts globally

Mobile banking adoption continues to scale globally, reaching 2.3 billion registered accounts. Of these, 593 million are active on a monthly basis, resulting in a 25.7% activity rate.

Up to 100% of adults in developed countries participate in banking systems

Banking penetration has reached near-universal levels in several advanced economies. Countries such as Denmark and Iceland report 100% participation, while others like Germany (99.98%), Austria (99.95%), and the United Kingdom (99.76%) are just behind.

Mobile banking transactions exceed $2.1 trillion

In 2025, mobile banking channels processed over $2.1 trillion, doubling in just four years. The increase in average transaction size indicates that users are relying on mobile banking for larger and more frequent financial activities.

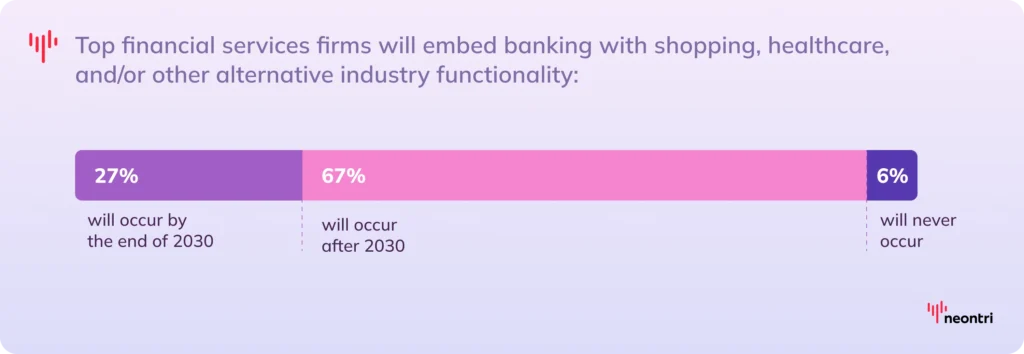

67% of global banking leaders expect embedded finance to redefine mobile banking

67% of executives believe that most top financial institutions will integrate banking into non-banking platforms by 2030. This will shift mobile banking from standalone apps to a background layer that powers experiences across e-commerce, mobility, and other digital ecosystems.

Mobile banking usage statistics

Mobile banking is now the dominant channel for everyday financial management, with user preferences shifting decisively toward digital-first interactions and personalized, on-demand experiences.

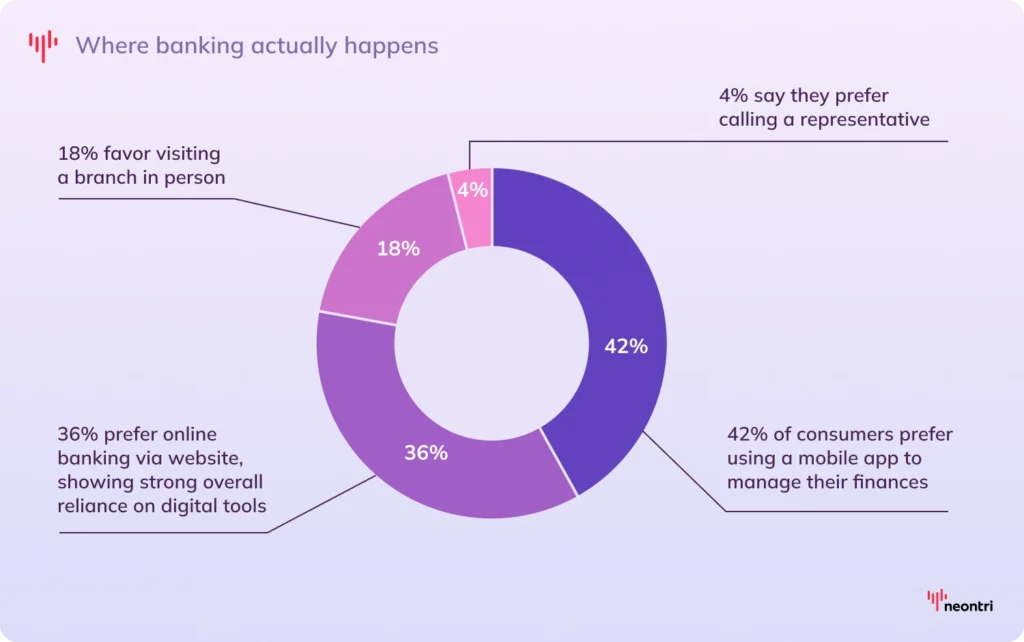

78% of consumers prefer digital banking over traditional channels

Digital banking has become the default method of managing personal finances. Mobile apps lead all channels, with 42% of consumers favoring them for everyday operations. 36% of users prefer to access banking services through websites, indicating that multi-channel digital access remains important.

Despite digital dominance, nearly one in five consumers still value in-person interactions and visit a branch for complex or high-trust transactions. Calling a representative is the least-preferred method, with only 4% choosing this option.

84% of consumers are satisfied with their mobile banking experience

Despite rising expectations and competitive pressure, mobile banking apps are largely meeting user needs, with 84% of consumers reporting satisfaction.

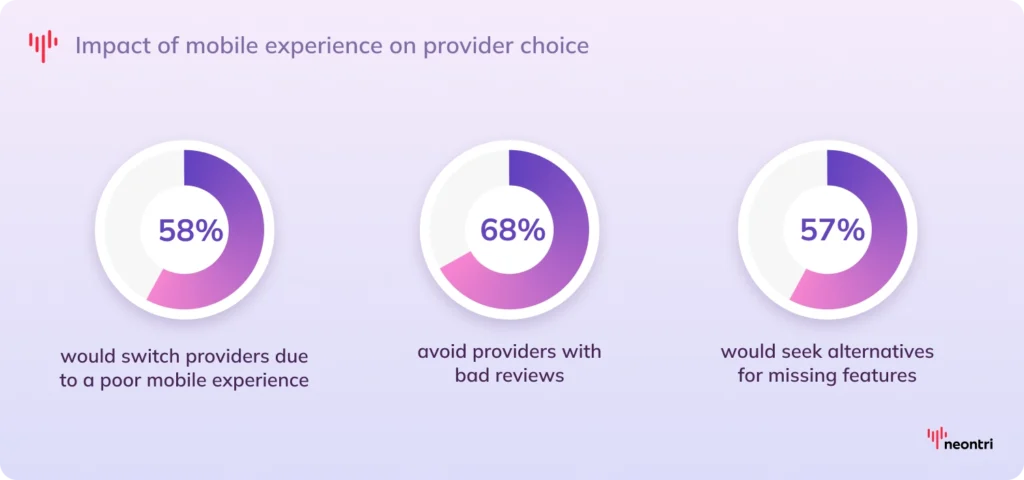

58% of consumers would switch providers due to a poor mobile experience

Around 58% of consumers say they would switch financial providers if the mobile experience is poor, while 67% would avoid choosing a provider altogether if it had low app ratings or bad reviews. In addition, 57% are willing to look for alternatives if their current provider fails to deliver key mobile features.

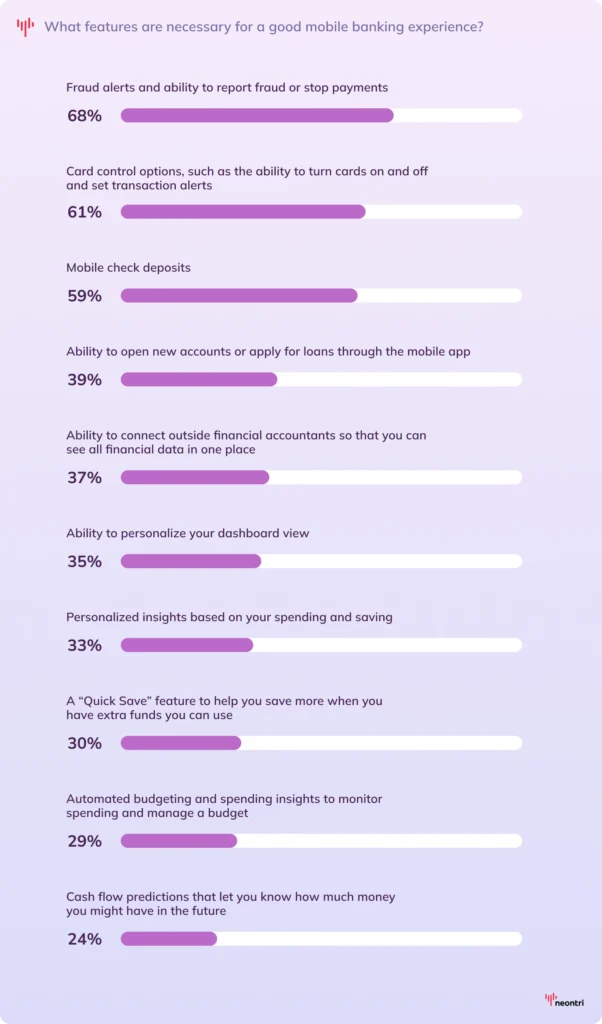

68% of users prioritize fraud alerts as the most important mobile banking feature

Fraud alerts and the ability to quickly report suspicious activity are the most important features for a strong mobile banking experience, cited by 68% of consumers. This is followed by card control options, such as the ability to turn cards on and off and set transaction alerts, valued by 61% of users, and mobile check deposit functionality, highlighted by 59%.

46% of consumers expect more personalization from mobile banking apps

Nearly half of users (46%) feel that current mobile banking apps fall short in personalization. The most requested features across all age groups are:

- financial education programs (42%)

- predictive insights into future account balances (33%)

- personalized recommendations to improve spending and saving habits (33%).

47% of consumers use three or more finance apps

Nearly half of consumers (47%) have at least three finance-related apps on their phones, highlighting a fragmented ecosystem where users combine banking, payments, and other financial tools.

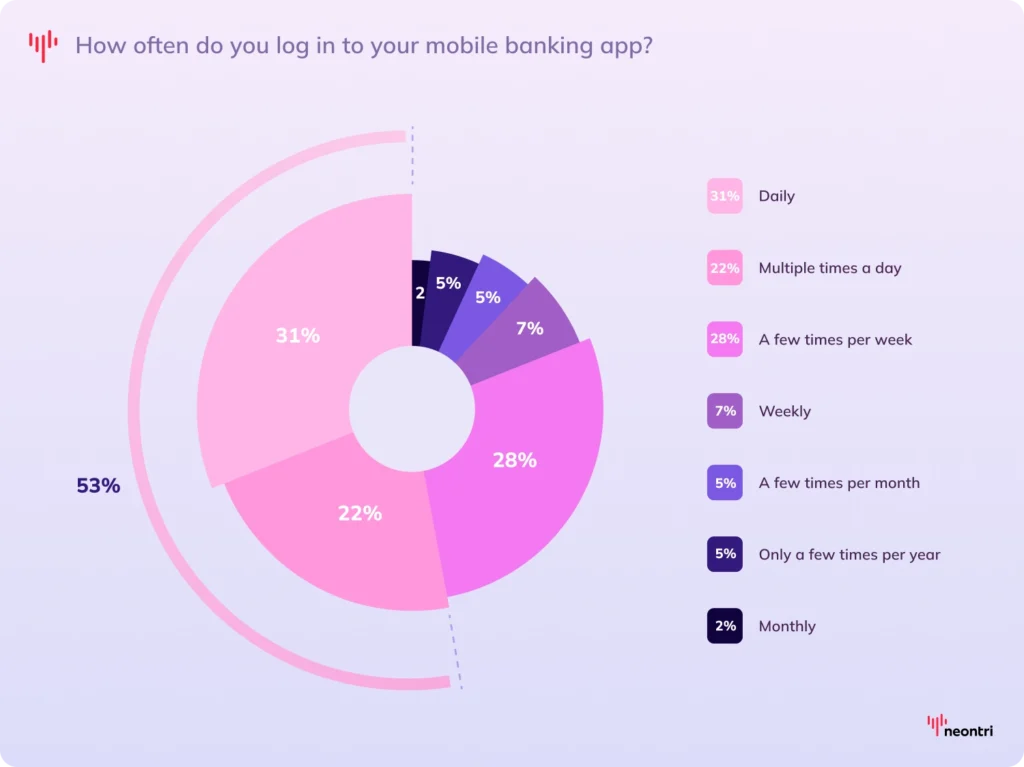

53% of users access financial apps daily

Around 31% of consumers log in at least once a day, while another 22% access their primary app multiple times a day.

57% of consumers want a single app for all finances

A majority of consumers (57%) say they would consolidate all financial accounts into one mobile app for easier management, yet only 13% have actually done so. Interest in all-in-one financial apps is even higher among younger generations, with 62% of Gen Z and 64% of Millennials willing to consolidate their finances into a single mobile platform, signaling where future adoption is likely to accelerate.

43% of banking leaders believe unified financial accounts will never fully replace separate products

The shift toward combining checking, savings, and credit into a single unified solution remains uncertain. While 21% bankers expect this model to emerge by 2030 and 36% believe it will happen later, the largest share (43%) thinks it will never occur, highlighting skepticism around the future of fully integrated mobile banking products.

Artificial intelligence in mobile banking adoption statistics

Artificial intelligence is no longer experimental in banking: leading institutions have already identified hundreds of AI use cases.

62% of consumers have yet to adopt AI in mobile banking

AI in mobile banking is still in an early adoption phase. Around 62% of consumers haven’t used any AI-powered financial tools. However, high satisfaction rates (70%) among existing users suggest strong latent demand once trust, awareness, and usability barriers are addressed.

Younger generations are driving AI adoption in financial apps

AI usage in mobile banking shows a clear generational divide. Millennials lead adoption, with 64% having tried at least one AI tool and 29% relying on them for financial decisions. Gen Z follows, showing growing comfort with AI-driven money management (25%) and key decision-making (20%). Adoption among older generations remains minimal, with only around 10% of Boomers and the Silent Generation having experimented with AI at all.

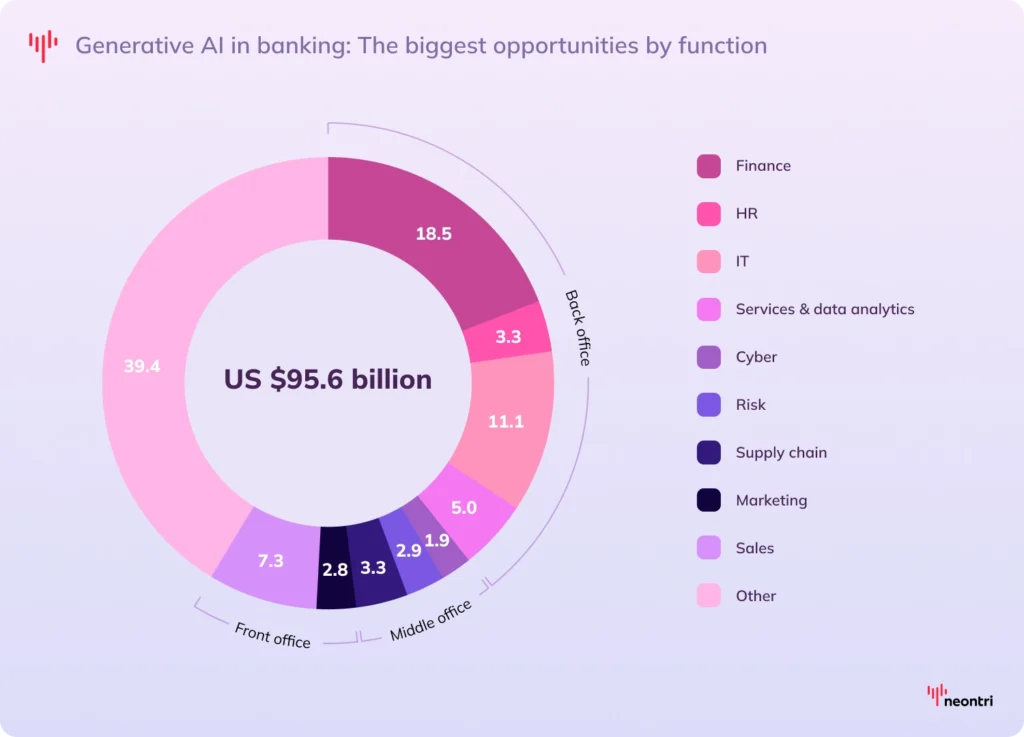

GenAI could unlock $95.6 billion in value across banking

GenAI in banking has an estimated value potential of $95.6 billion, with the largest impact concentrated in core functions. The three highest-value-generating business areas are finance with $18.5 billion, followed by IT at $11.1 billion and sales at $7.3 billion.

98% of banks expect GenAI to transform customer experience, but mostly after 2030

22% of financial institutions expect more than half of banks to deploy generative AI for customer experience by 2030, while a much larger share, 76%, believe this will happen later.

84% of institutions are exploring agentic AI capabilities

Banks are beginning to explore autonomous AI systems capable of performing multi-step tasks with minimal human intervention. This reflects the early stages of a move toward more self-directed, intelligent banking systems.

AI in mobile banking is led by simple, assistive use cases

Current adoption is concentrated around low-friction interactions. About 27% of users engage with AI through virtual assistants, primarily for support and quick queries within mobile apps. More advanced use cases, such as financial decision support (14%) and ongoing money management (13%), are emerging but remain less widespread.

AI adoption goals in banking are dominated by operational priorities

Leadership priorities for AI focus heavily on efficiency and risk reduction rather than long-term strategic value creation. The top goals include increasing operational efficiency (45%), enhancing customer experience (42%), and driving revenue growth (41%).

AI goals vs. actual benefits show a gap between ambition and realized value

The largest ambition-to-outcome gaps in banking appear in customer experience, where 42% of organizations have set it as a goal but only 27% report meaningful results. Revenue growth shows a similar mismatch (41% vs. 26%), and risk mitigation is not far behind (40% vs. 31%).

In contrast, operational efficiency is the closest to expectation, with 36% achieved against a 45% target, while financial planning remains fully balanced at 26% achieved versus 26% planned. Notably, stakeholder management is the only area in which outcomes exceed expectations, achieving 31% against a 29% goal.

Over 80% of banks still rely on on-premises systems and build AI solutions in-house

Control remains a key concern for banking leaders, with 58% expressing unease about the influence of external AI technology providers on their operations. This explains why 83% of banks continue to operate on-premises systems, while 86% develop AI solutions in-house.

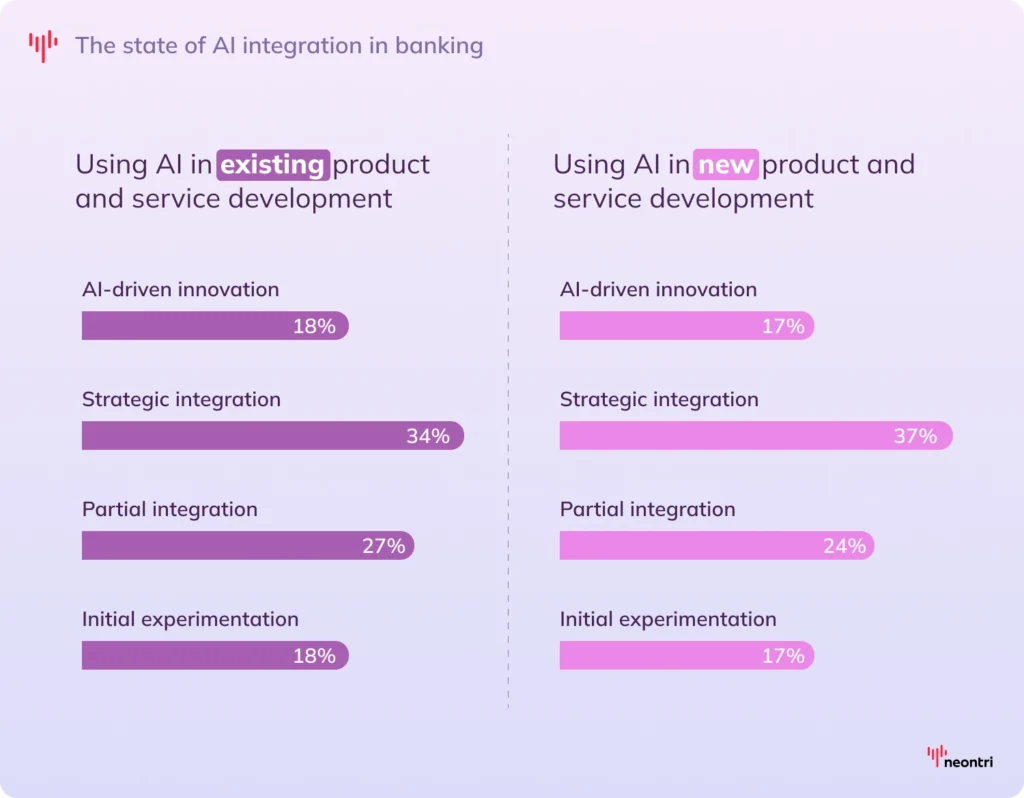

Only 18% of banks have reached advanced AI-driven innovation

Most banks are still mid-journey in AI integration. For existing products, 34% have reached strategic deployment, 27% remain in partial integration, and 18% are still running initial experiments. Only 18% report achieving full AI-driven innovation across their existing products.

The pattern holds almost identically for new product development: 37% are at the strategic integration stage, 24% are in partial integration, 17% are still experimenting, and just 17% are operating at full AI-driven innovation.

72% of banks cite data issues as a major AI adoption barrier

Nearly three-quarters of institutions report challenges with data quality, consistency, and accessibility, limiting the accuracy and effectiveness of AI models in production environments. Among specific integration challenges, banks often cite:

- security and data privacy concerns (38%)

- fragmented data environments (27%)

- inconsistent data formats (21%).

Trust remains a major barrier to AI adoption among banking clients

A combined 71% of consumers either do not trust AI (43%) or are unsure (28%) about using it to manage their finances. Trust levels vary across demographics: men (35%) are more likely to trust AI than women (23%), and Gen Z shows the highest confidence at 37%, though even within this group, skepticism still dominates.

Key technology trends shaping mobile banking

From cloud infrastructure and blockchain to AR/VR and super apps, mobile banking is being reshaped by a new wave of technologies that extend far beyond traditional app functionality.

Banks now run over 30% of their critical workloads in the cloud

60% of banks report migrating at least 30% of their critical workloads, including core banking platforms, data processing, and customer-facing services, to the cloud.

70% of banks expect to move the majority of their enterprise applications to the cloud

Over two-thirds of banking executives project that around 75% of their systems will be cloud-native by 2030.

82% of financial institutions rely on multi-cloud strategies

Cloud adoption in banking is evolving beyond single providers, with 82% of financial institutions operating in hybrid or multi-cloud environments. This shift accelerated in 2025, as enterprise multi-cloud deployments grew by 37% compared to the previous year.

Only 25% of banks have the cloud infrastructure needed for scalable AI

25% of banks currently operate on cloud or hybrid cloud platforms that can fully support data-driven services. This limits the ability to scale AI effectively and slows down the transition from pilot projects to enterprise-wide implementation.

Legacy systems and regulation remain key barriers to cloud adoption

While cloud migration unlocks significant growth potential, it remains a complex and resource-intensive process. 55% of institutions identify legacy infrastructure as the primary barrier to migration, while 46% point to regulatory compliance as a major challenge.

Cloud adoption cuts banking IT and infrastructure costs by up to 30%

Cloud transformation delivers immediate financial impact, including 20-30% IT cost reductions, a 27% drop in infrastructure expenses, and a 7.7% decrease in overall operational costs. At scale, this translates into massive savings of up to $2.4 billion annually by reducing reliance on on-premises systems and maintenance-heavy legacy infrastructure.

Only 32% expect VR/AR to reach meaningful adoption in banking by 2030

Only 32% of executives believe that even 20% of consumers will use VR/AR for transactions, reflecting cautious optimism. This skepticism largely stems from the fact that widespread adoption of these technologies depends on overcoming barriers such as development costs, specialized talent requirements, and user readiness.

50% of banking executives expect AR/VR to eventually break through

Half of financial leaders believe AR and VR will become a meaningful part of digital banking, even though current adoption remains limited. Early movers are already deploying AR-powered ATM locators and interactive 3D spending visualizations, while the next wave points toward virtual wealth management lounges, wearable-enabled interactions, and fully digital branches staffed by remote advisors.

Just 27% believe cryptocurrencies could rival cash by 2030

Confidence in crypto as a mainstream payment method remains low: only 27% of executives expect digital currencies to significantly replace cash, reflecting ongoing skepticism.

88% of merchants report customer demand for cryptocurrency payments

88% of merchants say customers have asked about paying with cryptocurrency, and 69% report that users want to use it at least once a month, highlighting growing expectations for crypto-enabled payment options.

Over 50% of users want core financial services integrated into super apps

Over half of consumers want mobile purchases (54%), money transfers (53%), and bill payments (51%) built directly into a single platform, making robust fintech integration the defining feature of the superapp experience.

56% choose super apps to save space on their devices

56% of users cite saving space on their smartphones as a key reason for using super apps, since they replace multiple standalone apps with a single integrated solution.

Super apps achieve up to 80% customer retention

While traditional banking apps retain around 50% of active users year over year, super apps can reach 70-80% retention, driven by their broader, everyday utility beyond financial services.

Find out what’s holding your mobile banking app back

A structured audit of an existing app uncovers friction points, performance gaps, and missed opportunities before your users do

Super apps deliver 40% higher user engagement than single-purpose apps

Engagement levels in super apps are substantially higher, with top platforms reporting around 40% higher engagement than standalone banking apps.

Super apps drive 2x product adoption per customer

Super app users often hold more financial products, frequently doubling the number of services used per customer compared to traditional banking apps.

Bottom line: Why the data is your roadmap

The numbers tell a clear story: mobile banking is no longer a feature – it is the primary battlefield for customer loyalty, revenue growth, and long-term relevance. Every percentage point of adoption, every second shaved off a transaction, and every personalized insight delivered in the right moment represents a real competitive edge for the institutions that get it right.

For banks and fintechs alike, these statistics aren’t just industry benchmarks to monitor. They are a strategic guide to understanding where to invest, which capabilities to prioritize, how to design mobile experiences that drive lasting customer value, and how to scale innovation without compromising trust or compliance.

References

https://www.fortunebusinessinsights.com/mobile-banking-market-114735

https://marketmindpartners.com/mobile-banking-market-252

https://hub.q2.com/resources/col/pf/2025-retail-banking-trends-and-priorities-report;

https://www.linkedin.com/pulse/case-study-worlds-first-mixed-reality-vr-ar-banking-ux-alex-kreger

https://assets.kpmg.com/content/dam/kpmg/ng/pdf/2025/intelligent-industries/Intelligent%20banking%20-%20Report.pdf

https://www.mx.com/research/the-missing-link

https://www.mx.com/research/crossing-the-chasm-consumer-demand-mobile-experiences

https://worldpopulationreview.com/country-rankings/mobile-banking-usage-by-country

https://www.gsma.com/sotir/wp-content/plugins/plugin_gsma_sotir/reports/The-State-of-the-Industry-Report-2026_English.pdf

https://www.codebtech.com/banking-superapps-a-strategic-whitepaper