Banks face an inflection point in identity verification: global fraud losses exceeded $12.5 billion in 2024, synthetic identity fraud increased 153% in the first half of 2024, and regulatory penalties reached $4.6 billion globally – yet only 4% of financial institutions have majority-automated KYC processes. The gap between compliance requirements and operational capability has never been wider, making the selection and implementation of effective KYC tools a strategic imperative for banking executives.

This article examines how modern KYC tools for banks address identity verification, AML compliance, and customer due diligence requirements while delivering measurable operational improvements. Whether evaluating automated KYC software for digital onboarding or strengthening sanctions screening capabilities, this analysis provides the technical depth and vendor intelligence necessary for informed decision-making.

Key takeaways

- Automated KYC tools reduce onboarding time by up to 94% and cut operating costs by up to 70%.

- AI-enhanced KYC platforms reduce false positives by 50-66%, allowing compliance teams to focus on genuine threats.

- Modern KYC solutions integrate multiple capabilities, including biometric verification, document verification, real-time sanctions screening, and risk scoring engines that provide explainable, auditable decisions.

What are KYC tools?

KYC tools for banks are specialized software platforms that automate identity verification, assess financial crime risk, and ensure regulatory compliance throughout the customer lifecycle. These solutions combine document verification capabilities, AML compliance tools, and risk scoring engines into integrated platforms that replace manual, paper-based processes with digital workflows.

Modern banking KYC platforms serve multiple functions: they verify customer identities through biometric and document analysis, screen individuals and entities against sanctions lists and PEP databases, calculate risk scores based on configurable parameters, and provide continuous monitoring to detect changes in customer risk profiles. The best solutions integrate seamlessly with core banking systems through REST APIs and SDKs while maintaining audit trails required by regulators.

Manual vs automated KYC

The contrast between manual and automated KYC approaches reveals stark differences in efficiency, accuracy, and cost. Manual KYC processes, still prevalent at many institutions, require customers to submit physical documents, wait for an analyst to review them, and endure onboarding timelines that can stretch from weeks to months. Fenergo’s research found that average KYC review times reached 95 days in 2023 – up from 84 days in 2022.

Manual processes also carry significant cost burdens. Corporate client KYC reviews average $2,598 per case, with annual spending at large financial institutions ranging from $60 to $175 million. These costs stem primarily from labor-intensive document collection, data entry, verification phone calls, and the back-and-forth communication that characterizes traditional onboarding.

Automated KYC solutions transform this equation entirely. According to FNZ, modern identity verification software completes document verification and biometric matching in under 35 seconds. Leading platforms achieve straight-through processing rates of 78% or higher, meaning the vast majority of low-risk customers complete onboarding without human intervention.

The accuracy differential proves equally significant. Traditional AML screening systems generate false positive rates between 42% and 95%, according to KYC2020 research. This requires analysts to investigate thousands of alerts that yield no suspicious activity. AI-enhanced automated systems reduce these false positives by 50-66%, dramatically improving productivity while ensuring genuine risks receive appropriate attention.

Why KYC processes are critical for banks

Regulatory enforcement has reached unprecedented intensity, making robust KYC processes essential for institutional survival. TD Bank’s $3.09 billion settlement in 2024 for systemic AML compliance failures demonstrates the scale of potential penalties. This follows the pattern established by Binance’s $4.3 billion settlement in 2023 and Goldman Sachs’ $2.9 billion 1MDB-related penalties – both stemming from inadequate customer due diligence and AML controls.

The regulatory landscape continues to expand. In the European Union, a comprehensive AML package adopted on May 31, 2024 introduces directly applicable regulations effective July 10, 2027. It establishes a new Anti-Money Laundering Authority (AMLA) headquartered in Frankfurt and increases maximum penalties to €10 million or 10% of total annual turnover. In the United States, FinCEN’s Customer Due Diligence Rule mandates identification and verification of beneficial owners, ongoing monitoring for suspicious activity, and maintenance of comprehensive customer risk profiles.

FATF Recommendation 10 requires financial institutions to prohibit anonymous accounts, verify customer identity when establishing business relationships, and apply enhanced due diligence to politically exposed persons (PEP), high-risk jurisdictions, and correspondent banking relationships. As a result, customers linked to the 21 countries currently on FATF’s grey list are subject to additional scrutiny, with banks reporting 20-30% higher onboarding costs and timelines extended by 3-6 weeks.

Beyond regulatory compliance, effective KYC tools address the fraud crisis threatening banking profitability. Account takeover fraud reached $15.6 billion in 2024, up from $12.7 billion in 2023. According to TransUnion, new account fraud totaled $6.2 billion, with synthetic identity fraud exposure for US lenders reaching an all-time high of $3.3 billion. Veriff reports that 1 in 20 verification attempts (5%) is now fraudulent, with fraud activity increasing 21% between 2024 and 2025.

Key features of KYC tools for banks

Effective banking KYC platforms integrate multiple capabilities into cohesive workflows that address identity verification, document verification, financial crime screening, and ongoing monitoring requirements.

Identity verification

Modern identity verification software employs multiple biometric technologies to establish customer identity with high confidence. Facial recognition remains the primary method, with AI algorithms matching facial images extracted from ID documents against live selfies. According to University of Michigan research, top systems achieve 95% deepfake detection rates, addressing the growing threat of AI-generated synthetic identities.

Liveness detection prevents spoofing attacks where fraudsters present photos, videos, or masks instead of genuine faces. Active liveness detection prompts users to perform specific actions – nodding, blinking, or head rotation – while passive liveness analyzes involuntary cues, including natural blinking, skin texture, and micro-expressions. Three-dimensional depth sensing creates face maps using laser scanners or structured light, providing accuracy 20-100x that of 2D matching, according to FaceTec.

Document verification

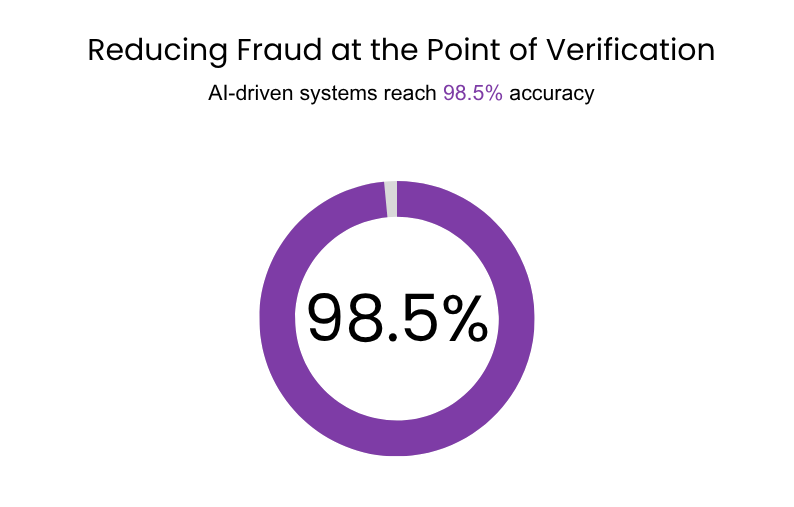

Document verification technology combines optical character recognition (OCR), machine learning classification, and fraud detection to authenticate identity documents. According to Markets Growth Reports, Modern AI-powered OCR achieves 98.5% accuracy.

The verification pipeline processes documents through multiple stages: image preprocessing for noise reduction and skew correction, automatic document-type classification, field extraction across languages, and cross-reference validation against government databases. NFC chip reading enables verification of cryptographically signed data embedded in ePassports and modern national ID cards, providing tamper-proof authentication that supplements visual document analysis.

Sanctions screening

AML compliance tools screen customers against global sanctions lists, PEP databases, and adverse media sources to identify financial crime risk. Primary data sources include the OFAC Specially Designated Nationals (SDN) list, the UN Consolidated List, the EU sanctions lists, and the UK HMT financial sanctions targets.

Leading vendors update sanctions lists every 60 minutes, ensuring banks screen against current designations. PEP databases contain over 1 million records globally, covering heads of state, government officials, judges, military personnel, and their family members and close associates. Adverse media screening monitors 60,000+ global news sources across 100+ countries, categorizing articles by risk themes including financial crime, regulatory violations, and reputational harm.

Fuzzy matching algorithms address the challenge of name variations across languages and transliteration systems. NLP-based technology handles diverse name phenomena, including nicknames, honorifics, spelling variations, and corporate name variations. Machine learning continuously improves matching accuracy, reducing false positives while preventing dangerous false negatives that could allow sanctioned entities to establish banking relationships.

Risk scoring

Risk scoring methodologies determine customer risk levels based on multiple factors, including geography, transaction patterns, source of funds, and business activities. Rules-based scoring applies predefined criteria – transaction thresholds, high-risk country connections, PEP status – to calculate initial risk ratings.

Explainability requirements from regulators mandate that risk scoring models provide clear rationales for customer ratings. The European Banking Authority requires interpretable, auditable, and understandable models. The EU AI Act classifies AI systems by risk level with corresponding regulatory requirements.

Effective KYC platforms provide visibility into which data points influenced risk scores, enabling compliance teams to defend decisions during regulatory examinations.

Customer onboarding workflow

Digital onboarding workflows orchestrate the complete customer acquisition process from initial application through account activation. Leading platforms offer no-code workflow builders that enable compliance teams to configure verification sequences without engineering resources.

Effective workflows incorporate conditional logic that adjusts requirements based on customer characteristics. Low-risk retail customers might complete basic identity verification through document capture and selfie matching.

At the same time, corporate clients trigger enhanced due diligence, including beneficial ownership verification, source-of-funds documentation, and multi-level approval processes. The goal is achieving straight-through processing rates of 50-65% for low-risk customers while applying appropriate scrutiny to higher-risk relationships.

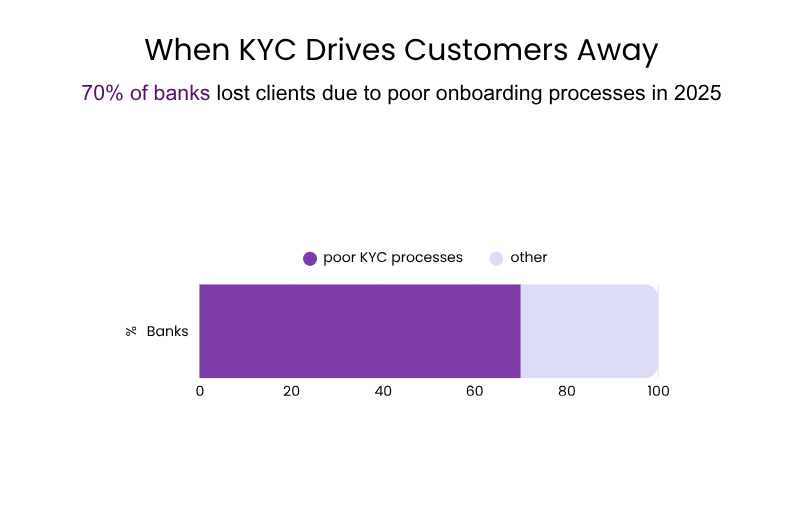

Fenergo reports that 70% of banks lost clients due to poor KYC processes in 2025 – a record high. Effective onboarding workflows balance compliance requirements against friction, with leading implementations completing verification in under 60 seconds for 95% of customers.

Ongoing monitoring

Continuous KYC (cKYC) and perpetual KYC (pKYC) replace traditional periodic reviews with real-time monitoring that detects changes in customer risk profiles as they occur. Historically, KYC reviews were performed every 1, 3, or 5 years, often allowing material changes in customer circumstances to go unnoticed between review cycles. Event-driven pKYC addresses this gap by triggering alerts when key risk signals emerge, such as sanctions list updates, adverse media coverage, changes in beneficial ownership, or shifts in transaction behavior.

The efficiency gains are significant. PwC estimates that pKYC can reduce KYC-related costs by 60-80% compared to periodic reviews, equating to approximately $14.4 million in annual savings for large institutions. At the same time, real-time monitoring strengthens risk management by identifying issues immediately rather than months or years later.

Integration and API capabilities

Modern KYC platforms provide RESTful APIs, mobile SDKs for iOS and Android, and web SDKs for browser-based integration. Response times average approximately 350 milliseconds for screening APIs, enabling real-time verification during customer onboarding. Batch processing capabilities support screening hundreds to thousands of records simultaneously for periodic portfolio reviews.

Pre-built integrations with core banking systems, customer relationship management platforms, and customer lifecycle management tools reduce implementation complexity. Webhook capabilities enable real-time notifications of verification status changes, supporting event-driven architectures. Normalized data models ensure consistent output formats across data sources and document types, simplifying downstream processing and analysis.

Benefits of using automated KYC software for banks

Automated KYC software delivers measurable gains across onboarding speed, operational costs, accuracy, and regulatory compliance. By replacing manual reviews with straight-through processing and real-time verification, banks improve both customer experience and risk control at scale.

| Benefit | Description |

|---|---|

| Faster onboarding (time-to-yes) | Automated KYC reduces onboarding times by up to 94%, with verification completed in seconds rather than days or weeks. For example, Monzo Bank cut verification from days to seconds using Jumio, onboarding over 2 million customers, while EQ Bank increased onboarding completion rates by 10% after implementing Trulioo. |

| Lower operating costs | By minimizing reliance on large teams for repetitive verification tasks, institutions reduce direct labor costs and overhead associated with manual identity checks and document handling. Industry data show that automation can cut manual labor costs by up to 70%, as banks shift routine tasks to software systems that operate at scale and in real time. |

| Improved accuracy and risk detection | AI-driven systems reduce false positives by 50–66%, allowing analysts to focus on genuine risks. “First-time-right” quality metrics improve by 15-40%, reducing rework and customer friction. Enhanced accuracy also lowers false negatives, minimizing the risk of undetected financial crime. |

| Stronger regulatory compliance | Automated KYC ensures consistent policy enforcement, real-time sanctions screening, and comprehensive audit trails. Automated documentation reduces gaps commonly flagged during regulatory exams, while continuous screening lowers exposure compared to periodic manual checks. |

Top 3 KYC tools for banks

Three vendors have established leadership positions in the banking KYC market, each with distinct strengths and ideal use cases.

Onfido

Onfido operates as part of Entrust’s Identity Security portfolio following its April 2024 acquisition. The Real Identity Platform verifies 2,500+ document types across 195 countries using the proprietary Atlas AI engine developed over 10+ years. Onfido’s ETSI certification makes it particularly strong for EU compliance requirements, including Qualified Electronic Signature (QES) capabilities.

The platform secures trust across the customer lifecycle by automatically verifying identities through a combination of award-winning document and biometric verification, trusted data sources, and passive fraud signals. It enables 95% of users to be onboarded in 10 seconds or less, while maintaining false rejection and false acceptance rates below 0.1%.

Example: Tesco Bank

Onfido provides a secure, mobile-first application process for Tesco Clubcard Pay+, replacing slow postal applications with a smooth digital experience. Using the Tesco Bank app, customers verify their identity by simply scanning a government-issued ID and taking a selfie. Onfido’s “glare and blur” detection and AI-powered biometrics then work in tandem to confirm the document’s authenticity and match it to the user’s face. This streamlined approach ensures that the applicant is the rightful, physically present owner of the ID, allowing customers to open an account anywhere, at any time.

Trulioo

Trulioo supports verification across more than 14,000 document types and 700 million verifiable business entities in 195 countries, making the platform particularly well-suited for combined person-and-business verification (KYB). This global coverage is complemented by screening against more than 6,000 watchlists, enabling consistent compliance across jurisdictions.

Enterprise adoption underscores this positioning. Trulioo’s strategic partnership with J.P. Morgan Payments for identity verification reflects trust at the highest tier of financial institutions. Furthermore, EQ Bank reported a 10% increase in onboarding completion rates following implementation.

Beyond traditional KYC and KYB, Trulioo is extending its identity infrastructure into emerging agent-led commerce. The company has joined Google’s Agent Payments Protocol (AP2) initiative, contributing its Digital Agent Passport and Know Your Agent (KYA) framework to establish a verifiable trust layer for agentic payments. This approach ensures that autonomous digital agents are authenticated, authorized, and accountable before transacting, addressing a critical gap in AI-driven payment ecosystems.

Example: J.P. Morgan

In late 2023, J.P. Morgan officially integrated Trulioo into its partner ecosystem to streamline global identity and business verification (KYB) for its payments business. By leveraging Trulioo’s massive data network, the bank provides its corporate clients with a single point of access to verify identities across 195 countries, a critical capability for secure cross-border transactions. This partnership allows J.P. Morgan to offer its clients a way to fight fraud and stay compliant without having to build separate verification stacks for every country in which they operate.

Jumio

Jumio earned Leader status in the inaugural 2024 Gartner Magic Quadrant for Identity Verification, reflecting its position as a leading provider of AI-powered identity intelligence. The platform has processed more than 1 billion identity verification transactions across 200+ countries, supporting large-scale, global financial services deployments.

In October 2024, Jumio introduced Liveness Premium, its most advanced biometric liveness detection solution to date, specifically designed to counter deepfake and injection attacks. It leverages patented technology that combines randomized color sequences with AI-driven analysis to confirm human presence in real time. This multi-layer defense extends beyond traditional presentation attack detection and has demonstrated measurable impact, with early adopters reporting over 30% more sophisticated fraud attempts being successfully intercepted.

Jumio’s broader security architecture combines advanced liveness detection, AI-driven fraud analytics, anti-spoofing technologies, and connected intelligence, supported by a patent portfolio of more than 300 issued patents and applications across nearly 100 patent families. This approach enables continuous adaptation to emerging attack vectors while maintaining low friction for legitimate users.

Example: Toyota Financial Services

Toyota Financial Services (TFS) in Colombia implemented Jumio to verify the identities of customers applying for vehicle financing remotely, helping protect them against identity theft and loan fraud. The platform handles the heavy lifting of ID document authentication and biometric “liveness” detection. It combines AI-powered ID and selfie verification with email/phone risk analysis to make instant, trusted decisions.

How to choose the best KYC tool for your bank

Selecting appropriate KYC software requires systematic evaluation across multiple dimensions aligned with institutional requirements and risk appetite.

Compliance requirements

Regulatory alignment forms the foundation of vendor selection. EU-focused institutions should prioritize vendors with ETSI certification and eIDAS support.

US banks require platforms that support compliance with the FinCEN CDD Rule, beneficial ownership verification, and BSA reporting integration. Institutions operating across FATF grey-list jurisdictions need robust, enhanced due diligence workflows and comprehensive sanctions screening.

The July 2027 application date for the EU’s AMLR and AMLD6 introduces new requirements, including expanded beneficial ownership verification, coverage of crypto-asset service providers, and alignment with AMLA technical standards due by July 2026. Vendor roadmaps should demonstrate preparation for these requirements.

Integration capabilities

Technical integration complexity directly impacts implementation timelines and total cost of ownership. Evaluate API documentation quality, SDK availability for mobile and web platforms, and pre-built integrations with existing core banking systems.

Webhook capabilities enable event-driven architectures that support real-time processing. Normalized data models simplify downstream integration by providing consistent output formats across data sources. Consider whether the platform supports the existing institution’s technology stack and architectural patterns.

Data security and encryption

Security certifications provide independent validation that vendors meet recognized industry standards. SOC 2 Type II certification, held by all leading vendors, verifies the effectiveness of controls related to security, availability, and confidentiality through ongoing third-party audits. ISO 27001 certification further demonstrates that a vendor operates a formal information security management system.

Data residency requirements can significantly influence vendor selection, particularly for institutions subject to GDPR or sector-specific regulations. It is essential to assess how customer data is stored and processed geographically, as well as the vendor’s ability to support regional hosting where required.

Encryption practices should be evaluated across the full data lifecycle, including encryption in transit using TLS and encryption at rest using AES-256. In addition, data retention and deletion policies must align with regulatory obligations, including defined retention periods and support for the right to erasure under applicable data protection laws.

Automation level

Straight-through processing rates are a key indicator of potential operational efficiency gains. Vendors should be able to provide benchmark data based on institutions with comparable customer profiles, risk levels, and geographic exposure.

It is equally important to assess the balance between automation and accuracy. Over-automation without appropriate risk controls can increase false negatives, allowing sanctioned entities or fraudulent identities to pass verification.

The most effective platforms use risk-based, graduated verification – automating low-risk cases while applying additional checks only when risk signals are detected – rather than applying uniform processing to all customers.

Customization and workflows

Workflow customization capabilities enable alignment with institutional risk appetite and regulatory requirements. No-code workflow builders allow compliance teams to configure verification sequences without engineering dependencies. Evaluate whether conditional logic supports differentiated treatment based on customer type, geography, product, and risk indicators.

White-label capabilities matter for institutions prioritizing brand consistency in customer-facing interfaces. Evaluate customization options for UI elements, color schemes, messaging, and verification flow sequencing.

Implementation tips for banks

Implementing a KYC platform effectively requires a structured approach that balances technical complexity, regulatory compliance, and operational continuity. The following practices are critical for success:

- Comprehensive requirements gathering

Document regulatory obligations, existing workflows, integration points, and success metrics. Engage stakeholders across compliance, operations, technology, and customer experience to ensure all requirements are captured. Identify pain points in current processes.

- Phased deployment

Roll out the platform gradually, starting with a single product line or customer segment. This approach enables learning and adjustment before full-scale implementation while delivering early wins that build stakeholder confidence.

- Data quality preparation

KYC platforms depend on accurate customer data for verification and screening. Address data quality issues in source systems before migration to avoid propagating errors into the new platform.

- Change management

Compliance analysts accustomed to manual processes require training on new workflows and systems. Communication should emphasize how automation eliminates tedious tasks rather than threatening roles, enabling analysts to focus on higher-value investigation and analysis.

- Parallel operation during transition

Plan for parallel operation during transition periods. Running new and legacy systems simultaneously ensures continuity while validating new platform performance. Define clear criteria for cutover decisions and rollback procedures if issues emerge.

- Post-implementation optimization

Initial configurations based on pre-deployment assumptions rarely prove optimal. Analyze verification results, false positive rates, and processing times to identify tuning opportunities. Leading implementations achieve break-even within 4-9 months with ongoing optimization extending returns.

Future trends in KYC for banking

Several technological and regulatory developments will reshape banking KYC over the coming years.

Trend #1: AI risk scoring

AI-driven risk scoring adoption is accelerating dramatically. Machine learning models demonstrate 20% false positive reductions while improving the detection of novel money laundering patterns that rules-based systems miss. Explainable AI requirements from regulators will drive continued development of interpretable models that provide clear rationales for risk decisions.

Trend #2: Biometrics

Behavioral biometrics add continuous authentication layers that detect unauthorized access and social engineering attacks. Technology analyzes approximately 2,000 behavioral elements per session, including typing patterns, mouse movements, and touchscreen interactionsh. Use cases in banking include account takeover prevention, mule account detection, and identifying customers acting under duress during fraudulent transfers. The passive nature of behavioral biometrics adds security without customer friction.

Trend #3: Privacy-preserving solutions

Privacy-preserving technologies, such as zero-knowledge proofs and decentralized identity frameworks, allow organizations to verify information without exposing the underlying personal data. Use cases include proving age without revealing a birthdate, confirming income ranges without disclosing exact salaries, and validating credentials without sharing full identity details.

Trend #4: eIDAS 2.0

eIDAS 2.0 represents the most significant near-term regulatory development for European banking. Adopted on February 29, 2024, the regulation requires each EU member state to issue at least one EUDI Wallet by December 31, 2026, with mandatory acceptance by all relying parties, including financial institutions, by November 2027. The European Commission targets 80% active adoption by 2030. For banks, the regulation enables streamlined cross-border account opening, strong user authentication conceptually aligned with PSD2’s SCA requirements, and the elimination of physical documents for identity verification.

Trend #5: RegTech consolidation

RegTech consolidation continues as vendors expand their capabilities through acquisitions and strategic partnerships. The market is increasingly bifurcated between comprehensive platforms that provide end-to-end solutions and orchestration layers that enable multi-vendor integration. Banks are showing a growing preference for platforms that simplify vendor management while avoiding dependency on a single provider.

Conclusion

As KYC platforms continue to mature, their role extends far beyond compliance. Leading solutions now combine automation, advanced biometrics, real-time monitoring, privacy-preserving verification, and orchestration across multiple vendors to deliver seamless customer experiences while mitigating risk. Regulatory developments like eIDAS 2.0, FATF updates, and evolving AML obligations, alongside the rise of agentic payments and privacy-first identity frameworks, make KYC infrastructure an essential strategic investment.

Investing in modern KYC today positions banks to stay ahead of regulatory requirements, exceed evolving customer expectations, and turn compliance into a driver of competitive advantage.