The modern banking landscape is defined by the massive streams of data flowing through digital ecosystems. Big data analytics allows financial institutions to transform this raw information into actionable intelligence that helps anticipate market shifts with remarkable accuracy.

In this article, we’ll explore how financial institutions are using big data analytics to personalize customer journeys, fortify security, expand product offerings, and streamline internal operations. We’ll also cover the implementation challenges and how to address them, drawing on Neontri’s 13+ years of hands-on experience building banking software.

Key takeaways:

- Leading global banks, such as BNP Paribas, JPMorgan Chase, and ICBC, are transforming themselves into data-driven organizations by embedding big data analytics at the core of their operations.

- Big data analytics enables banks to enhance credit risk assessment, improve customer segmentation, develop targeted products, manage risks more effectively, make well-informed business decisions, and increase operational efficiency.

- Major challenges in implementing big data analytics include legacy systems integration, cybersecurity concerns, data quality issues, skill gaps in data science, and ethical considerations around data usage.

- Partnering with experienced technology providers like Neontri can help banks navigate the complexities of implementing big data analysis.

The importance of big data analytics in banking

The digital revolution has ushered in an age where data is not just an asset but the lifeblood of financial institutions. Consider this: the global population will create around 211 zettabytes of data by the end of the year.

The banking sector contributes a lot to that figure. The rapid growth of digital services, particularly online banking platforms and mobile apps, generates enormous volumes of behavioral data with every click, transaction, and customer interaction. To turn this torrent of information into something useful, banks are increasingly investing in sophisticated analytics platforms and artificial intelligence solutions designed to transform raw data into actionable insights in real time.

This is where big data analytics comes in. In a banking context, big data analytics refers to collecting, processing, and analyzing vast amounts of data to gain valuable insights that drive decision-making and strategy across financial institutions. It encompasses everything from customer transaction histories and behavioral patterns to market trends and regulatory compliance data.

The scale and diversity of this data is what sets big data analytics apart from traditional reporting. Rather than working with structured snapshots of historical performance, banks can now harness streaming data from multiple sources simultaneously, enabling them to detect fraud in milliseconds, personalize products in real time, and anticipate customer needs before they are expressed. In an industry where speed, accuracy, and trust are everything, the ability to act on data intelligently has become one of the most powerful competitive advantages a bank can have.

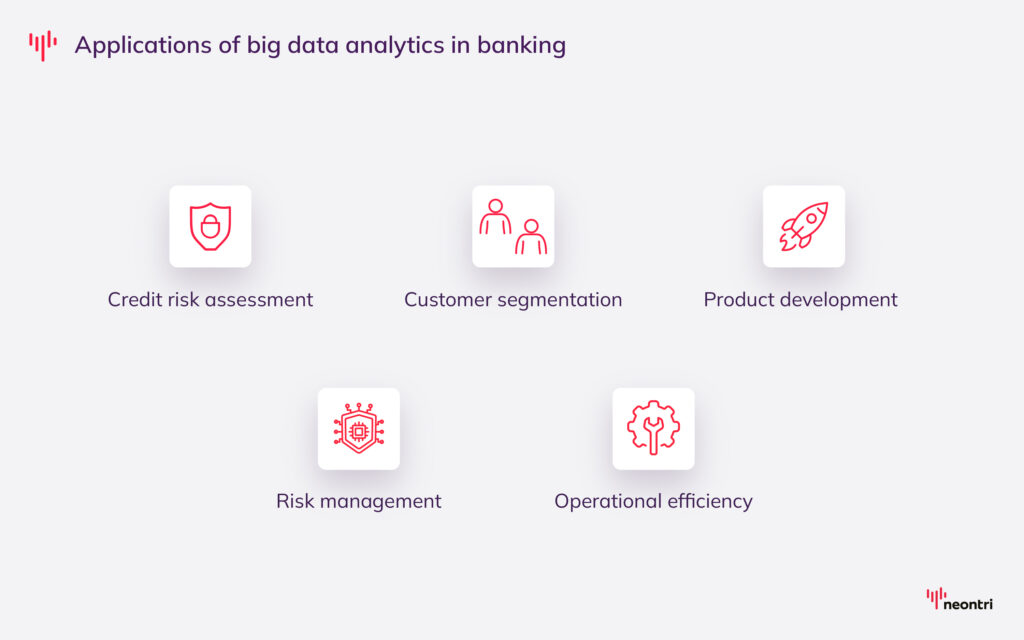

Big data analytics for banking: Top 5 use cases

Big data analytics offers a wide array of applications that enhance banking operations. These use cases demonstrate how financial institutions leverage data to assess credit risk more accurately, segment customers for targeted engagement, drive smarter product development, strengthen risk management frameworks, and unlock new levels of operational efficiency.

Use case #1: Smarter credit scoring for a more inclusive banking future

Financial institutions often exclude potential borrowers due to limited credit history. Big data processing is changing that, enabling banks to expand their customer base by revolutionizing how creditworthiness is assessed. Rather than relying solely on traditional credit scores, banks can now build far more comprehensive risk profiles by drawing on a broader range of alternative data sources.

This approach has proven particularly valuable for reaching underserved segments, including young adults, immigrants, and small business owners who lack conventional credit histories. For example, innovative fintech companies use mobile phone data, such as contacts, social media activity, and geographical patterns, to create alternative credit scores, enabling instant loan approvals for individuals whom traditional banks and credit unions would typically deny.

To further optimize these processes, banks are also leveraging advanced AI credit scoring solutions that deliver faster and more accurate assessments. This data-driven approach not only helps banks tap into new market segments but also promotes financial inclusion while maintaining prudent risk management practices.

Use case #2: Building leaner, smarter banking operations with big data

By leveraging large datasets and advanced analytics techniques, banks can streamline key processes, reduce costs, and improve overall performance across various operational areas. In back-office operations, bottlenecks that once went undetected can now be promptly identified and resolved. For example, by analyzing the flow of loan applications across departments, banks can pinpoint where delays typically occur and implement targeted improvements before they affect the customer experience.

Beyond process optimization, big data analytics plays a central role in workforce planning, resource allocation, and vendor management, giving institutions a clearer picture of where time and capital are being spent. These capabilities form the backbone of successful digital transformation initiatives in banking, enabling organizations to move away from legacy inefficiencies and build leaner, more agile operations.

Use case #3: Personalized banking through smarter customer segmentation

In modern retail banking, customer segmentation has evolved into a sophisticated, data-driven process. This approach enables banks to create personalized services that drive customer satisfaction and loyalty while maximizing profitability. Here’s how the process typically unfolds:

- Data gathering. Banks collect a wide array of customer data, including: demographic data, account activity and product usage, past interactions and declined offers, life events and milestones, spending patterns and service preferences.

- Data clean-up. Raw data is cleaned and standardized to ensure accuracy and consistency across all data points.

- Data mining. Advanced algorithms sift through the cleaned data to identify patterns, correlations, and insights that might not be apparent through simple analysis.

- Data analysis. Through big data analysis, banks can create detailed customer profiles with unprecedented precision, which helps them tailor products and services to different demographic segments. By examining historical customer data and transaction histories, banks can identify patterns in spending habits and channel preferences (online, mobile, or in-person). This insight enables targeted marketing campaigns and personalized service offerings.

- Algorithmic forecasting. By leveraging machine learning algorithms, banks can forecast clients’ future behavior and needs. This proactive approach allows financial institutions to anticipate customer requirements and offer relevant solutions before they’re requested.

Use case #4: Data-driven product innovation in banking

By harnessing vast amounts of customer data, banks can create highly targeted and innovative financial products that address specific customer pain points. The process begins with comprehensive data mining, where banks analyze behavioral patterns, spending habits, and financial goals to identify gaps in their current offerings and uncover emerging market opportunities.

Big data analytics also enables banks to anticipate customer needs before they fully materialize. By examining market conditions, demographic shifts, and technological advancements, institutions can take a forward-looking approach to product design. For example, the rise of cryptocurrency among Gen Z prompts banks to use big data insights to develop secure digital wallets and crypto-investment products tailored to this tech-savvy generation, staying ahead of demand rather than simply reacting to it.

Use case #5: Big data analytics for smarter operational risk management in banking

Operational risk management is a critical banking function, and the implementation of big data has significantly improved this process. By analyzing internal banking data, customer complaints, and external events, banks can identify potential operational vulnerabilities before they escalate.

Here are some examples of risk management capabilities of big data analytics in banking:

- Stress testing. Banks can run complex simulations using vast amounts of historical and real-time data to better prepare for a wide range of potential economic scenarios and regulatory changes.

- Customer churn. Big data analysis in banks can help identify which client types are most at risk of leaving by spotting indicators such as negative survey feedback or decreased product usage. This enables proactive engagement strategies, like targeted offers or personalized communication, to retain at-risk customers.

- Predictive maintenance. Banks can predict when maintenance is needed before breakdowns occur by analyzing usage patterns and performance data from ATMs and other banking equipment. This allows banks to implement preventative measures, schedule maintenance during off-peak hours, and ensure backup systems are in place.

- Market fluctuations. Advanced algorithms can detect subtle patterns and correlations across global markets, helping banks to anticipate market movements and adjust their trading strategies accordingly. This capability is crucial in today’s volatile financial markets, where split-second decisions can significantly impact investment portfolios.

Building the foundation for data analytics with Neontri: Real bank case study

Implementing big data analytics at scale is not just a technology decision – it’s an architectural one. Each of the main banking business models requires an IT infrastructure capable of handling significant variations in demand for streaming and processing capacity, making careful system design and implementation essential from the outset.

That’s where the right partner makes all the difference. With 13+ years of experience in custom banking software development, cloud development, and data management, Neontri can be a perfect technology partner on this journey. Our company specializes in near-real-time data analytics, empowering organizations to unlock the true value of their data as it streams in.

Our partnership with PKO Bank Polski puts that expertise into perspective. As Poland’s largest commercial bank and one of the leading financial institutions in Central and Eastern Europe, PKO Bank Polski operates at a scale where security, reliability, and performance are business-critical.

Challenge: PKO Bank needed a high-performance data management system capable of handling massive transaction volumes without compromising speed, reliability, or scalability.

Solution: Neontri’s banking engineering team developed an enterprise-grade data management system built on a 72-node cluster architecture, engineered to handle PKO’s most demanding operational requirements while remaining fully scalable for future growth.

Outcome: The system processes up to 10,000 transactions per second with an average data retrieval speed of just 55ms. Daily operations now include 200-500 million record offloads, 50 million data retrievals, and a total daily offloading volume of 19TB, meeting both current demand and long-term scalability needs.

Key benefits of big data analytics in retail banking

From improving customer care to preventing fraud, big data analytics empowers banks to transform raw information into valuable insights. This technological advancement has not only modernized individual banking operations but has also reshaped the entire financial services landscape, ushering in an era of more convenient, personalized, and secure digital solutions.

Benefit #1: Personalized banking through 360-degree customer insights

Big data analytics collects information from various data points, including online banking activity, service interactions, and even social media engagement. This helps banks create 360-degree customer profiles and gives them a holistic view of customer behavior, preferences, and needs.

By codifying, unifying, and centralizing key analytics and supporting processes, banks can offer personalized services and a much better user experience. The business case is compelling: research by McKinsey shows that financial institutions that invest in personalizing their services generate 40% more revenue. This increase is largely driven by more effective up-selling and cross-selling opportunities, and the ability to deliver the right financial products to the right customers at the right time.

Example: BBVA analyzes millions of customer transactions to provide personalized financial health recommendations in real time. Using data on income, expenses, debt, savings, and spending habits, the bank identifies each customer’s financial profile and offers tailored plans – such as debt reduction, savings improvement, or long-term investment strategies. Automated alerts detect unusual financial events and trigger timely suggestions to help customers stay on track with their goals.

Benefit #2: Advanced analytics for fraud prevention and risk assessment

Modern analytics platforms enhance fraud prevention and risk assessment capabilities. By analyzing transaction history and unusual behavior, they can spot illegal activity, helping banks avoid potential losses.

Example: HSBC monitors and scores millions of transactions in real time, analyzing patterns to identify fraudulent activity within one second of a transaction request. The bank protects approximately 30 million cards globally, using analytical models that continuously adapt to detect evolving threats. This approach has achieved significantly lower fraud rates while minimizing false positives that could anger legitimate customers.

Benefit #3: Reducing banking costs through big data automation

Big data analytics offers significant cost-saving benefits for banks. By automating routine data-driven tasks, such as compliance reporting, credit assessments, and customer due diligence, banks can dramatically reduce the manual effort and operational overhead traditionally associated with these processes.

Example: A large multinational bank partnered with Dell Technologies to consolidate data silos and modernize traditional reporting tools, creating a unified data platform. Within less than a year, the bank onboarded all 3,000 data analytics experts and consolidated fragmented data systems to create a single, unified data view with employee self-service access. This transformation enabled automated, accurate reporting, resulting in $4.1 million in cost-avoidance savings from incremental investment in compute and storage infrastructure over three years.

Benefit #4: Smarter banking decisions through integrated data reporting

By drawing on data from multiple sources simultaneously, banks can generate more comprehensive, accurate, and insightful reports that reflect the true complexity of their business. These documents provide a deeper understanding of financial market trends, customer interactions, and day-to-day operations, leading to better strategic planning and sharper competitive positioning

Moreover, advanced visualization tools can translate complex data into easily digestible formats that non-technical stakeholders can act on. This helps break down the silos that often slow decision-making, ensuring every department, from risk to marketing to operations, works from the same informed baseline.

Example: JPMorgan Chase transformed its reporting capabilities by implementing enterprise-wide analytics, expanding from 400 users in 2011 to nearly 215,000 users today across over 500 teams. The bank reduced manual reporting time from months to weeks, saving thousands of hours and improving enterprise-wide decision-making through greater transparency. This allows its employees, from analysts to C-level executives, to quickly answer business questions without waiting for IT, while maintaining rigorous governance through documented data dictionaries and verified data sources that meet security control guidelines.

Benefit #5: Using big data to build smarter, more efficient branch networks

Branch network optimization powered by big data helps banks cut costs and maximize returns by aligning resources with actual customer needs. By analyzing foot traffic, transaction volumes, and demographics, financial institutions can make data-driven decisions about branch locations, staffing levels, and service offerings. This might lead to the closure of underperforming branches, the introduction of digital-first initiatives, or the reallocation of resources to high-potential areas, ensuring every investment drives measurable value.

Example: TD Bank uses GIS technology and data science to identify optimal branch locations by analyzing hundreds of factors, including drive times and online banking usage patterns. The system accurately predicts potential deposits for new locations, replacing intuition-based decisions with data-driven site selection that better serves customer needs.

Benefit #6: Data-driven innovation in banking products and services

By leveraging big data analytics, banks can identify market trends and unmet customer needs, enabling them to create innovative products and services. Data-driven insights allow banks to make informed decisions about product development, marketing strategies, and service delivery, helping them maintain their competitive edge in a rapidly evolving industry.

Example: Barclays has embedded big data analytics across virtually every part of its organization, from developing customer propositions to fraud detection and cybersecurity. To bolster its capabilities, the bank has recently signed a multi-year strategic deal with S&P Global, securing full access to the Capital IQ Pro platform and its research, data, and analytics spanning equities, fixed income, credit, and derivatives. The deal gives Barclays access to data quality and scale that would be difficult to build independently, accelerating innovation and enabling the kind of deep market insight its clients increasingly expect.

Navigating the challenges of big data analytics in banking

As the banking services sector embraces digital transformation, banks face several challenges in effectively implementing and leveraging big data analytics. By understanding and proactively addressing data integration barriers, financial institutions can better position themselves to harness the full potential of big data technologies while minimizing risks and maintaining customer trust.

Challenge #1: Protecting banking data in an evolving cyber threat landscape

Finance is the second-most targeted sector for cyberattacks globally, with the average cost of a data breach reaching $5.56 million, well above the cross-industry average. According to IBM, 53% of data breaches involve customers’ personally identifiable information, including tax identification numbers, emails, phone numbers, and home addresses, which can be used in identity theft and credit card fraud.

Attackers are deploying increasingly sophisticated methods, from AI-generated phishing campaigns to ransomware targeting core banking infrastructure, that outpace traditional defense mechanisms. Consequently, banking institutions face relentless pressure to safeguard sensitive assets against an evolving threat landscape. To mitigate these risks, leading banks are no longer treating security as a peripheral concern; instead, they are prioritizing cybersecurity and robust data protection as the indispensable foundational elements of their broader big data strategies.

Challenge #2: Overcoming data silos and dirty data in financial analytics

Maintaining high data quality across different sources remains a significant challenge for financial institutions venturing into big data analytics. Poor quality data, often called “dirty data”, can lead to flawed analysis and misguided business decisions, with inaccuracies, inconsistencies, and outdated information quietly undermining even the most sophisticated analytical frameworks.

The presence of data silos further complicates matters, as valuable insights often remain trapped within departmental boundaries. This fragmentation prevents a holistic view of information and directly impacts the bottom line. Gartner estimates that poor data quality costs on average $12.9 million annually per organization – an expense that compounds across every layer of decision-making.

Challenge #3: Managing the risks of unstructured data

Gartener estimates that 70-90% of all data is unstructured, making it difficult to analyze and derive meaningful insights. This data comes from diverse sources, including social media interactions, customer emails, website browsing patterns, and contact customer service – all generating different kinds of information from the same customer across multiple touchpoints.

What makes this challenge particularly acute is that most organizations are overestimating their ability to manage it. Despite 75% of organizations expressing confidence in their ability to secure unstructured data, 68% simultaneously report that a significant portion of that data remains unprotected, and a further 10% are unsure of their actual coverage. For banks handling sensitive customer and transaction data at scale, that gap between confidence and reality isn’t just an operational blind spot – it’s a serious liability.

Challenge #4: The talent gap in banking data analytics

Data analysts are essential for managing, analyzing, and interpreting the wealth of data generated by banks to extract actionable insights. Their ability to transform raw information into strategic advantages makes data science expertise invaluable for financial institutions.

However, attracting, retaining, and growing the talent pool for these skills is daunting, given the high demand. Industry projections indicate a 34% growth in demand for data-centric roles across different sectors in 2024-2034. This translates to roughly 23.4K openings for data scientists each year over the decade.

In addition to this fierce competition for talent, banks face an additional challenge as they require professionals who not only possess technical expertise but also understand the unique regulatory and operational complexities of the financial sector. This dual requirement significantly reduces the pool of suitable candidates, intensifying the competition for experienced engineers and potentially slowing the adoption of big data analytics in banking.

Challenge #5: Legacy infrastructure: A barrier to big data adoption in banking

One of the most pressing challenges for banks is their reliance on outdated infrastructure that wasn’t designed to handle the volume and complexity of modern big data solutions. These legacy systems often lack the capability to perform advanced analytics, forcing banks to either upgrade their existing infrastructure or undergo a complete system overhaul.

On top of that, the cost of inaction is fast outpacing the cost of modernization. According to an IDC study, banks that fail to modernize legacy systems could lose over $57 billion by 2028. Compounding the problem, legacy systems already consume the bulk of IT budgets in most financial institutions, leaving little room to invest in future-ready technologies.

Ready to modernize your banking systems?

Challenge #6: Building customer trust through responsible data use

As clients become increasingly concerned about how their personal information is being used and protected, building and maintaining customer trust remains a critical challenge. Banks must ensure that their data collection and analysis practices respect individual privacy rights and comply with evolving global regulatory standards, such as the GDPR and the EU AI Act.

Customers and regulators alike are demanding greater visibility into how data-driven decisions are made, particularly in high-stakes areas like loan approvals or fraud flagging, where an unexplained automated decision can have significant real-world consequences. Ultimately, banks must strive for fairness, ensuring that their systems don’t lead to discrimination against certain groups or individuals.

Leading the future: Banks shaping big data innovation

Across the global banking landscape, leading institutions are redefining what it means to be data-driven. These banks are not merely adopting analytics tools – they are embedding big data into the core of their business models to gain sharper insights, improve efficiency, and deliver hyper-personalized customer experiences. Below, we look at how some of the industry’s most forward-thinking institutions are putting data to work.

JPMorgan Chase

JPMorgan Chase approaches big data analytics as a strategic engine for both innovation and resilience. With more than 150 petabytes of data spread across 30,000 databases, the bank has built one of the world’s most advanced analytics ecosystems, integrating AI-driven models, cloud computing, and real-time processing to extract actionable insights at scale.

The bank’s Hadoop-based infrastructure processes vast volumes of unstructured data, including emails, social media posts, phone calls, and transaction records that traditional databases cannot handle. This capability enables JPMorgan to optimize foreclosed property sales, develop targeted marketing initiatives, and conduct sophisticated risk assessments by identifying hard-to-detect patterns in financial markets and customer behavior.

For JPMorgan, data is not just about operational efficiency; it is about contextual intelligence. The bank’s analytics systems are designed to deliver the right product to the right customer, through the right channel, at the right time. This extends across multiple domains: from detecting fraud through advanced pattern recognition, to supporting cash management with predictive forecasting, to enriching customer experiences with context-aware payment insights.

JPMorgan is the first financial institution to leverage big data analytics for the public good. The firm uses de-identified customer transaction data to help policymakers better understand the U.S. economy in real time, bridging gaps left by slower government surveys. By treating data as a living asset that powers decisions across risk, compliance, customer engagement, and societal impact, JPMorgan sets a benchmark in how financial institutions can transform analytics into a measurable advantage.

BNP Paribas

As the largest bank in the Eurozone, with 178,000 employees and nearly 30 million clients, BNP Paribas generates massive volumes of data daily through customer transactions, online banking interactions, and operational activity. But rather than viewing data as a byproduct of business, the company treats it as a strategic resource that fuels every aspect of performance, from customer insight to operational precision.

Through the years, the bank has developed sophisticated internal systems that convert vast, complex datasets into actionable intelligence. These capabilities have revolutionized processes across customer engagement, marketing, branch management, and risk oversight.

By integrating visualization and analytics tools, the bank has accelerated analysis timeframes from weeks or months to minutes or seconds. Geographic analytics enables precise segmentation by income and risk profiles, allowing hyper-targeted marketing and the strategic placement of ATMs based on customer density and competitor presence. Real-time monitoring of branch performance tracks key metrics, including customer acquisition, retention, and profitability, empowering managers to act swiftly, seize opportunities, and resolve challenges as they arise.

These examples represent just a fraction of how BNP Paribas leverages big data analytics across its operations. Looking ahead, the bank envisions an even deeper integration of data capabilities into its core identity. With a commitment to becoming increasingly technology-driven, BNP Paribas is investing in next-generation analytics infrastructure, expanding its community of over 3,000 data specialists, and fostering partnerships with innovative technology companies.

ICBC

Industrial and Commercial Bank of China (ICBC), one of the world’s largest banks by assets and market value, has become a leader in applying big data analytics to transform its operations. With hundreds of millions of retail and corporate clients, ICBC recognized the value of data-driven decision-making early on.

Since the mid-2000s, it has built one of the most advanced big data infrastructures in global finance. This comprehensive system integrates data lakes, data warehouses, and group information databases through a three-layer architecture spanning source, aggregation, and extraction levels. Operating at unprecedented scale, the platform supports over 50,000 active users internally, feeds more than 100 downstream systems, and powers over 1,000 business scenarios – handling what the bank claims is the industry’s largest capacity and most diverse range of data types.

The platform employs machine learning, combined with expert rules, for data classification, protection, and lifecycle governance. It uses graph databases to build knowledge maps linking data assets, sources, indicators, and tags. This sophisticated infrastructure has delivered tangible business results, helping the bank acquire 1.4 million retail customers and 900,000 corporate clients through enhanced marketing precision and data integration.

ICBC’s big data applications extend across critical banking domains, including the following:

- In fraud prevention, the bank’s independently developed ICBC e-Security system has cumulatively intercepted 250,000 instances of telecom fraud and recovered 5.8 billion yuan in financial losses for customers through real-time monitoring across all channels – from physical outlets to mobile banking.

- In credit risk management, the bank established the industry’s first specialized Credit Risk Monitoring Center. It leverages big data to conduct real-time scanning and multidimensional analysis to identify previously missed exposures and to avoid potential losses exceeding 10 billion yuan.

- In marketing, the bank leverages analytical models that monitor customer behavior patterns to enable intelligent product recommendations and targeted campaigns with closed-loop management tracking.

- In performance management, big data analytics provide comprehensive visibility into each branch’s performance, departmental resource consumption, employee value output, product costs, and customer business contributions.

Looking ahead, ICBC continues to enhance its big data capabilities by integrating external data sources from government departments, international organizations, and information service providers, while exploring models to quantify and potentially monetize data assets as the regulatory framework for data exchange and trading evolves.

Big data analytics tools in banking: What to use and when

Choosing the right big data analytics tools is one of the most consequential decisions a bank can make – and with the market expanding rapidly, the options can be overwhelming. Whether building custom banking data platforms or integrating off-the-shelf solutions, financial institutions need to match the right tools to their specific use case, budget, and technical capacity. The table below breaks down the five most common tool categories to help navigate that decision.

| Tool category | Examples | Best for | Typical cost range | Implementation complexity |

|---|---|---|---|---|

| Data lakehouse | Databricks, Snowflake | Unified analytics and machine learning | $50K-500K/yr | High |

| Stream processing | Kafka, Flink | Real-time fraud detection | $20K-200K/yr | Very High |

| Data warehouse | Redshift, BigQuery | Structured reporting | $30K-300K/yr | Medium |

| Business intelligence and dashboards | Tableau, Power BI | Executive reporting | $10K-100K/yr | Low-Medium |

| ML platforms | SageMaker, Azure ML | Predictive models | $15K-150K/yr | High |

Final words

Big data analytics is no longer a future ambition for banks – it’s a present-day operational necessity. From personalizing customer journeys and detecting fraud in real time to streamlining internal operations and driving smarter product development, institutions that harness their data effectively are the ones setting the pace for the rest of the industry.

The technology, the tools, and the expertise exist today. The only question is how quickly your organization is ready to move. If you’re looking to build a data analytics capability that’s tailored to the demands of modern banking, get in touch with Neontri experts and let’s build it together.

FAQ

How can big data analytics drive innovation in the banking sector?

Big data analytics enables organizations in the banking industry to identify emerging market trends and unmet customer needs, leading to the development of innovative financial products and services.

How does big data help banks comply with regulatory requirements?

By leveraging advanced analytics, banking institutions can monitor customer data for suspicious transactions and perform real-time screening against sanctions lists and PEP databases, ensuring compliance with anti-money laundering and counter-terrorism financing regulations. The technology also streamlines customer due diligence, enables automated reporting and documentation, and facilitates risk assessment and management, allowing banks to maintain their operations in line with regulatory requirements.

Can big data analytics enhance the accuracy of lending decisions?

Big data analytics in the banking industry significantly improves lending decisions by analyzing alternative data sources beyond traditional credit scores, such as social behavior, utility payments, and even mobile phone usage patterns. This allows banks to better assess creditworthiness, especially for borrowers with limited credit history.

What is the role of machine learning in big data analytics in banking?

Machine learning algorithms process vast amounts of banking data to identify patterns, predict customer behavior, and automate decision-making.

What are the key benefits of real-time data processing in investment banking?

Real-time data processing enables investment banks to make faster, more informed decisions regarding trading and risk management. It allows continuous monitoring of market movements, portfolio exposures, and liquidity positions, helping firms react instantly to market changes. This agility not only enhances profitability and risk mitigation but also improves client service through up-to-the-minute insights and precise execution.

What’s the difference between big data analytics and traditional banking business intelligence?

Traditional banking business intelligence focuses on structured, historical data, like predefined dashboards, scheduled reports, and queries that answer questions already known in advance. It operates on a relatively narrow slice of available data, typically drawn from core banking systems and transaction records.

Big data analytics operates on an entirely different scale. It ingests massive volumes of data from a far broader range of sources, including customer interactions, social media activity, IoT devices, third-party data feeds, and processes it in real or near-real time. Rather than simply reporting on the past, it uncovers patterns, predicts future behavior, and can trigger automated decisions without human intervention.

Should a mid-size bank build or buy its big data analytics stack?

For most mid-size banks, a hybrid approach makes the most sense — buying proven infrastructure components such as cloud data warehouses while building custom layers to address specific business logic and compliance requirements. Building everything in-house demands significant time, talent, and capital that most mid-size institutions can’t justify.

Sources

- https://helpware.com/blog/customer-experience-trends-in-banking

- https://www.businesswire.com/news/home/20260331632063/en/Unstructured-Data-Surges-as-Enterprises-Struggle-to-Maintain-Visibility-and-Security-Cloud-Security-Alliance-Study-Finds

- https://www.gartner.com/en/data-analytics/topics/data-quality

- https://thefintechtimes.com/legacy-tech-cost-banks-57billion-in-2028-idc-finds/

- https://www.ibm.com/downloads/documents/us-en/131cf87b20b31c91

- https://documents1.worldbank.org/curated/en/505891573224492672/pdf/Using-Big-Data-to-Expand-Financial-Services-Benefits-and-Risks.pdf

- https://www.bls.gov/ooh/math/data-scientists.htm

- https://www.bbva.com/en/financial-health/how-bbva-uses-data-to-look-after-its-customers-financial-health/

- https://www.sas.com/content/dam/SAS/en_gb/doc/CustomerStories/hsbc.pdf

- https://www.esri.com/about/newsroom/publications/wherenext/ali-abedini-of-td-bank

- https://www.tableau.com/solutions/customer/jpmorgan-chase-chooses-tableau-enable-self-service-analytics-keeping-rapid

- https://www.delltechnologies.com/content/dam/uwaem/production-design-assets/en-gb/connected-finance/assets/cost-reduction.pdf

- https://www.aidataanalytics.network/business-analytics/news-trends/barclays-sp-global-sign-multi-year-data-analytics-deal

- https://www.projectpro.io/article/how-jpmorgan-uses-hadoop-to-leverage-big-data-analytics/142

- https://www.jpmorgan.com/content/dam/jpmorgan/documents/technology/jpmorganchase-emerging-technology-trends-a-jpmorganchase-perspective.pdf

- https://group.bnpparibas/en/our-commitments/innovation/data-artificial-intelligence

- https://group.bnpparibas/en/news/data-bnp-paribas-strategy

- https://www.theasianbanker.com/updates-and-articles/icbc-launches-new-data-platform-to-enhance-business-integration-and-reduce-redundancy

- https://www.icbc-ltd.com/icbc/en/newsupdates/icbc%20news/ICBCUsesBigDatatoEffectivelyProtectCustomersMoneyBags.htm