The financial services industry stands at a pivotal crossroads. For senior banking executives across North America and Europe, the challenge is unmistakable: approve more qualified borrowers, reduce default rates, and maintain strict regulatory compliance—all while modernizing legacy underwriting systems that are increasingly unable to keep pace.

In this high-stakes environment, AI credit scoring has emerged as a transformative solution, fundamentally reshaping risk assessment and lending processes. By leveraging advanced analytics and real-time data, these systems enable institutions to make faster, fairer, and more accurate credit decisions. For the time-constrained executive, the message is clear: adopting AI credit scoring is no longer a future consideration—it is an immediate business imperative.

This article provides a comprehensive roadmap for understanding, evaluating, and implementing AI credit scoring. It demonstrates how AI-powered systems deliver superior outcomes across the core challenges facing modern lenders, while offering actionable insights from Neontri experts in banking software development for building a resilient, scalable, and competitive lending strategy

Key takeaways:

- By analyzing a far broader and deeper set of data, AI models improve default prediction accuracy by 15-25%, allowing institutions to approve more loans while simultaneously lowering credit losses.

- AI-powered automation dramatically reduces processing times from days to minutes, cutting operational costs by decreasing the need for manual review by up to 60%.

- The ability to accurately assess thin-file borrowers using alternative data unlocks new revenue streams from previously unscoreable market segments, fostering financial inclusion and expanding the institution’s customer base.

Exposing the fault lines: The inherent limitations of legacy scoring

For decades, the financial industry has relied on traditional credit scoring models. Their analytical lens is narrow, relying almost exclusively on a limited set of historical data points from credit bureaus, primarily payment records, balance-to-limit ratio, and the length of an individual’s credit history.

This backward-looking, limited-data approach creates two significant problems. First, it is ill-equipped to accurately assess the creditworthiness of a large and growing segment of the population. “Thin-file” borrowers, including new-to-credit individuals, recent immigrants, and many small and medium-sized enterprises (SMEs) with limited formal credit histories, are often unfairly penalized or deemed unscorable by these legacy systems.

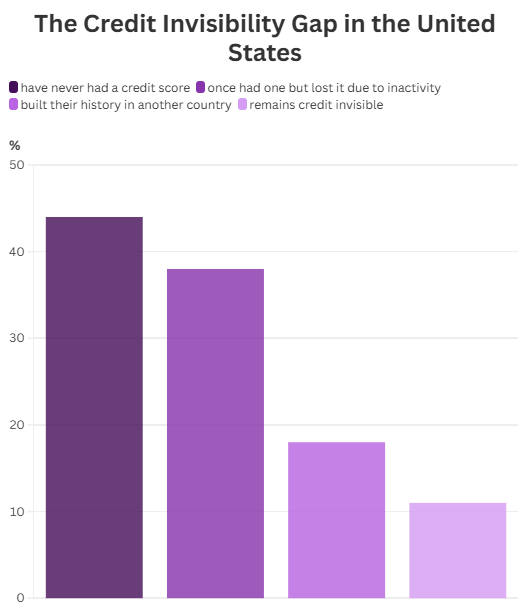

This represents a massive, underserved market and a significant missed opportunity for growth. In the U.S. alone, 28 million people have no credit record at all. 44% have never had a credit score, 38% once had one but lost it due to inactivity, and 18% built their history in another country. Altogether, about 11% of the population remains credit invisible—a gap that AI, through the use of alternative data, is beginning to close.

Second, these models are too rigid to keep up with changing economic conditions or shifting consumer behaviors. Every time a new trend emerges, human experts must manually create and add new rules—a process that is slow, costly, and inefficient. Over time, this builds into a tangled web of rules, making it unclear which factors actually drive outcomes. Without the ability to dynamically recalibrate, institutions face greater exposure to unexpected risks and miss out on emerging opportunities—a serious weakness in today’s fast-moving economy.

Build future-ready solutions

Move beyond static rules and unlock real-time credit intelligence with Neontri.

The evolution of credit scoring in the digital era

Lending is no longer a commoditized service; it is a primary battleground for customer acquisition and retention. Modern borrowers, conditioned by digital-native experiences in other sectors, now expect loan decisions that are not only fast but also fair and personalized.

The traditional 24-48 hour wait for manual application reviews is no longer acceptable. Competitors, particularly agile fintech companies, are raising expectations by providing approvals in minutes—setting a new benchmark that established lenders cannot afford to ignore.

What’s really shaking things up in lending right now isn’t just new players, it’s the technology they’re using. While traditional credit assessment methods falter amid uncertainty, fintechs are using AI to analyze alternative data sources, process applications in seconds, and spot risks that a human might miss.

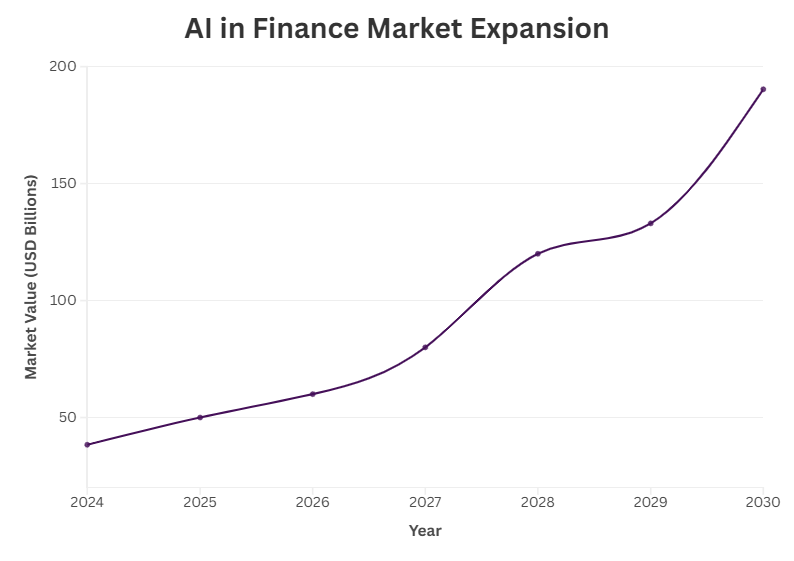

The global AI credit scoring market is experiencing unprecedented expansion, projected to grow at a CAGR of 25.9% from 2024 to 2031. This growth is situated within a much larger technological transformation: the broader “AI in finance” market is forecast to surge from an estimated $38.36 billion in 2024 to $190.33 billion by 2030, demonstrating the immense capital and strategic focus being directed toward these capabilities.

The push toward rapid adoption is not simply driven by technological promise, but by the visible shortcomings of traditional lending models. This acceleration highlights a critical reality: investing in AI is not just about improving efficiency, but about creating a more resilient and forward-looking risk management framework for the future.

Deconstructing AI credit scoring: Beyond the hype

At its core, AI credit scoring applies machine learning to estimate the likelihood that a borrower will default on a loan. Unlike traditional models that rely on linear regression and a handful of variables, AI models use techniques such as gradient boosting, random forests, and neural networks. These methods can analyze thousands of data points at once, uncovering non-linear patterns and subtle correlations in an individual’s financial behavior that conventional approaches cannot detect.

For example, instead of grouping borrowers into broad demographic categories, AI creates personal risk profiles. A traditional model might place someone in a “high risk” bucket based on age, income, or payment history. By contrast, an AI model builds a dynamic, multi-dimensional view of each customer, based on a holistic analysis of their unique financial activities.

For institutions seeking a sustainable competitive edge, success depends not only on adopting AI tools, but also on custom ML model development tailored to their specific risk appetite, product mix, customer segments, and regulatory environment. Off-the-shelf scoring solutions can accelerate experimentation, but custom-built models offer greater flexibility, transparency, and long-term strategic value for banks aiming to modernize underwriting at scale.

To make that choice more concrete, the table below compares the main AI credit scoring model types by use case, performance potential, explainability, and implementation complexity.

| Model type | Best for | Typical accuracy vs FICO | Data requirements | Explainability | Implementation complexity |

|---|---|---|---|---|---|

| Model type | Best for | Typical accuracy vs FICO | Data requirements | Explainability | Implementation complexity |

| Logistic regression | Regulated lending, explainability-first | +5–10% AUC | 12–24 months history | High (coefficients) | Low |

| Gradient boosting (XGBoost, LightGBM) | Most banking use cases | +15–25% AUC | 24+ months history | Medium (SHAP) | Medium |

| Neural networks | Complex pattern detection, large portfolios | +20–30% AUC | 36+ months, large dataset | Low (black box) | High |

| Random forest | Legacy data, fast deployment | +10–15% AUC | 18+ months history | Medium | Low–medium |

| Transformer / LLM-enhanced | Alternative data integration | +25–35% AUC | Mixed-source data | Variable | Very high |

| Ensemble (hybrid) | Production banking | +20–30% AUC | 24+ months + alternative data | Medium | High |

While traditional models are confined to the limited data provided by credit bureaus, AI-powered systems can integrate a far richer set of inputs, drawing on verified alternative data sources that paint a complete picture of a borrower’s financial life. Examples include:

- Authenticated bank transactions: Analyzing categorized income streams, recurring expenses, discretionary spending habits, and savings patterns reveals true repayment capacity.

- Cash-flow patterns: Assessing the volatility and timing of cash flows offers insights into financial stability, especially for gig economy workers or SMEs with irregular income.

- Utility and rent payments: A consistent history of paying rent, electricity, and telecom bills is a powerful indicator of financial responsibility that is often missing from credit files.

- Behavioral indicators: Permissioned financial data can reveal patterns in account management and financial discipline that correlate with creditworthiness.

By combining these signals into a holistic financial identity, AI models can accurately assess borrowers who remain invisible to traditional scoring methods. This does not necessarily replace traditional credit scores, but it enriches them with layers of predictive insight that produce far more granular and precise assessments.

This expanded view of creditworthiness also marks a deeper shift in risk management philosophy. Traditional scorecards provide only a static snapshot of past behavior, confirming reliability based on historical data. AI models, by contrast, with their capacity for continuous learning and real-time data ingestion, deliver adaptive predictions. They can forecast whether a borrower will remain reliable next month based on cash flow changes detected just days earlier. This allows institutions to anticipate and mitigate potential defaults before they occur, rather than simply documenting them afterward.

| Feature | Traditional credit scoring | AI credit scoring |

|---|---|---|

| Data sources | Relies on limited credit bureau data, application information, and historical patterns. | Incorporates credit history plus authenticated bank transactions, real-time cash-flow data, and a broad range of verified alternative data sources. |

| Model architecture | Employs static scorecards with predetermined variables and fixed weights, requiring manual updates. | Utilizes dynamic machine learning algorithms (e.g., gradient boosting, neural networks) with continuous model updates and adaptive learning. |

| Decision speed | Often involves batch processing and manual review, with turnaround times of 24-48 hours or more. | Enables real-time decisioning with response times in minutes or even seconds for a high volume of applications. |

| Risk assessment | Groups applicants into broad demographic segments, offering limited individual-level customization. | Generates precise, individual-level predictions based on a comprehensive analysis of unique behavioral and financial patterns. |

| Scalability | Scales linearly, requiring proportional increases in underwriting staff to handle higher application volumes. | Achieves exponential scalability through automated processes and intelligent workflows, allowing for massive growth in lending capacity without a corresponding increase in headcount. |

Benefits of AI-based credit scoring

The main reason for AI adoption for credit scoring stems from its proven ability to deliver measurable business results. Institutions that adopt it see sharper risk assessment, faster and leaner operations, and access to entirely new customer segments.

In other words, AI does not just enhance decision-making—it directly improves profitability, competitiveness, and long-term growth. By moving beyond theoretical benefits to hard data, executive leaders can build a compelling business case for investment.

Precision in risk management

The primary function of any credit scoring system is to accurately separate creditworthy borrowers from those likely to default. In this regard, AI models demonstrate a decisive superiority over traditional methods. By analyzing a more comprehensive dataset, they identify subtle risk indicators that legacy systems miss, leading to more precise predictions and a healthier loan portfolio. This advantage translates into measurable outcomes across several business areas:

- Predictive accuracy. Financial institutions implementing AI models report a 15-25% increase in default prediction accuracy compared to their traditional scorecards. A study by Lyzr shows that AI can reduce overall default rates by as much as 30%.

- Capturing bad debt. In a case study featuring a UK high street bank, an AI model successfully identified 83% of the bad debt that was not caught by traditional scores, drastically reducing the organization’s exposure to credit risk.

- Early warnings. AI transforms risk management from a reactive to a proactive discipline. Advanced AI-powered Early Warning Systems (EWS) can detect signs of financial distress in a borrower’s account 60 to 90 days earlier than traditional monitoring methods. According to Deloitte, some of these systems can identify emerging risks 9 to 18 months earlier than legacy EWS, giving organizations an extensive time for mitigation and intervention.

Efficiency through hyper-automation

AI credit scoring is a powerful engine for operational efficiency. With AI, routine applications can be automatically assessed and approved without human intervention. This significantly reduces the workload of underwriting teams and accelerates decision-making, with approval times cut by up to 90% for low-risk customers. For higher-risk or more complex applications, AI provides detailed analysis to guide human judgment, striking the right balance between efficiency and oversight.

The result is a system that can process far greater volumes of applications while delivering faster, more consistent decisions. This, in return, leads to:

- Massive cost savings. Autonomous Research projects that AI technologies could reduce operational costs for financial services companies by up to 22%, which would amount to global savings of more than $1 trillion by 2030.

- Reduced manual workload. When AI automates over 70% of routine applications, it frees credit officers from the mundane task of rubber-stamping standard auto or personal loans. This allows them to focus their expertise on high-value, complex cases—structuring sophisticated commercial loans, managing high-risk portfolios, or navigating nuanced credit situations where human judgment is irreplaceable.

- Faster decisioning. Loan application processing times are cut from days to minutes, and in many cases, to mere seconds, creating a vastly improved customer experience and a significant competitive advantage.

Expanding market access

By enabling faster, fairer, and more inclusive lending, AI empowers financial institutions to reach customers who were previously underserved or excluded. This not only strengthens trust and loyalty but also opens entirely new market segments. As lending becomes more accessible and responsive, institutions gain the dual advantage of expanding market share while reinforcing their reputation as forward-thinking and customer-centric.

AI unlocks entirely new lending opportunities. By incorporating alternative data, AI-based scoring can increase loan approval rates by 20–30% for individuals who were previously “unscorable” under traditional methods. In fact, one study found that a bank could expand lending to 77% more people while maintaining its existing default rate simply by switching to a more accurate AI model.

The combined effect of these improvements goes far beyond operational savings. It represents a powerful compounding impact on profitability. The real value lies not just in reducing underwriting costs, but in strategically reallocating skilled human capital—freeing experienced teams to focus on higher-value decisions, portfolio growth, and innovation.

Quantifiable ROI of AI-based credit scoring

The specific benefits of AI credit scoring manifest differently depending on the institution’s scale and strategic priorities. The following table segments the tangible impact to provide a more targeted view of the value proposition for different types of organizations.

| Benefit category | Enterprise-level institutions (5,000+ employees) | Medium to large businesses (1,000-5,000 employees) | Small to medium companies (50-1,000 employees) |

|---|---|---|---|

| Operational efficiency | -Automated loan risk assessment contributes to sector-wide savings of over $1 trillion by 2030. -Straight-through processing rates increase to 70-83%. -Manual review needs fall by 45-60%. | -Reduced time-to-market for new credit products through rapid model deployment. -Enhanced customer experience via faster approval processes. | -Drastically reduced processing times allow for competition with larger players. -Ability to scale lending volume without proportional staff increases. |

| Risk management | -Default prediction accuracy increases by 15-25%. -Early warning systems detect account stress 60-90 days earlier. | -Proactive risk management through continuous monitoring of borrower health. -Improved accuracy reduces overall portfolio risk and credit losses. | -Access to sophisticated risk assessment capabilities without building large internal data science teams. |

| Competitive positioning | Ability to serve previously unscoreable market segments -Potential to expand the customer base. | -Integration of alternative data enables lending to thin-file and SME borrowers. | -Partnership opportunities with third-party fintech providers for enhanced capabilities. -SME-specific provisions in regulations like the EU AI Act can reduce compliance burdens. |

Strategic implementation across the credit lifecycle

The impact of AI in credit assessment extends well beyond the initial loan decision. Its greatest value emerges when applied across the entire credit lifecycle, creating a continuous, data-driven feedback loop that strengthens risk management, deepens customer engagement, and drives efficiency from underwriting through to collections and recovery.

Use case #1: High-fidelity cash-flow underwriting

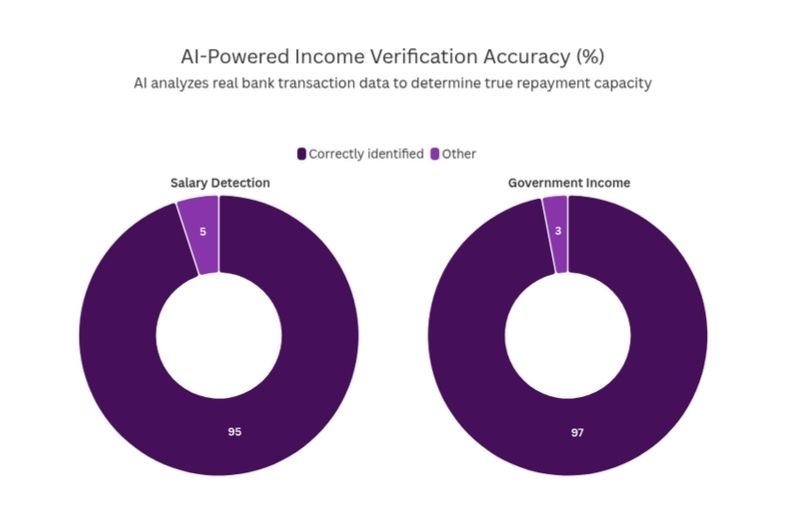

Traditional income verification methods are often manual, slow, and dependent on borrower-provided documents, such as pay stubs and tax returns, making the process tedious for both lenders and applicants. AI-powered systems streamline this by directly analyzing authenticated and categorized bank transaction data, offering a granular and objective view of the borrower’s true repayment capacity.

These models demonstrate exceptional precision, with documented accuracy rates of 95% in identifying salary streams and 97% in detecting government income sources. By factoring in recurring obligations, discretionary spending, and cash-flow volatility, AI delivers a more reliable picture of financial health than a simple credit score ever could.

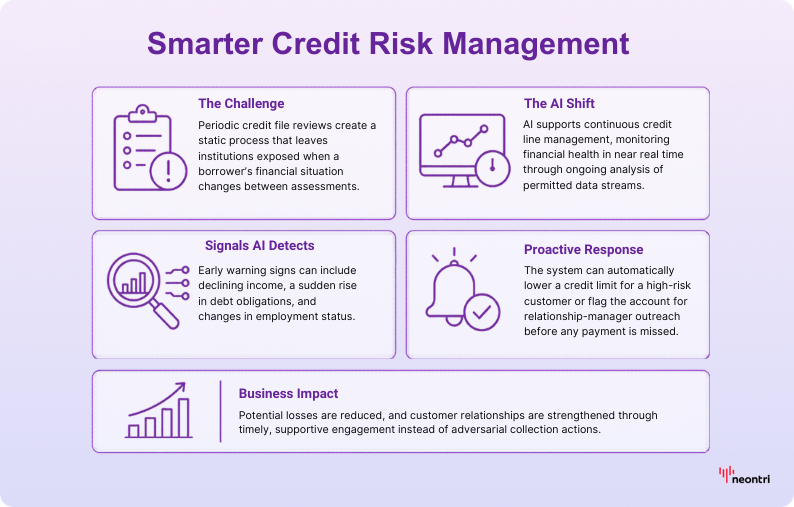

Use case #2: Continuous credit line management

Legacy credit management relies on periodic, often annual, reviews of a borrower’s credit file. This static approach leaves institutions vulnerable, as the client’s financial situation can deteriorate between assessments. AI enables a more dynamic model: continuous credit line management, where financial health is monitored in near real time.

By analyzing permissioned data streams on an ongoing basis, AI systems can detect early warning signals of distress, such as declining income, a sudden increase in debt obligations, or changes in employment status. This allows for proactive risk management interventions.

For instance, the system might automatically lower a credit limit for a high-risk customer or flag an account for outreach by a relationship manager—long before a payment is ever missed. The result is twofold: potential losses are reduced, and customer relationships are strengthened through timely, supportive engagement rather than adversarial collection actions.

Use case #3: Optimizing collections and recovery

The insights generated by AI credit scoring models continue to deliver value long after a loan is disbursed. Banks are increasingly using their capabilities to optimize collections and recovery. Rather than applying a one-size-fits-all strategy, AI integrates advanced scoring analytics directly into collections workflows.

Predictive models can prioritize delinquent accounts based not only on the amount owed but also on the probability of repayment and the expected recovery amount. This enables collections teams to focus their efforts where they will be most effective.

Furthermore, AI supports smarter treatment strategies by matching the most appropriate action—whether a reminder text, a phone call, or a formal letter—to each borrower’s circumstances and behavioral profile. This data-driven approach improves recovery rates while helping ensure that collection practices remain both fair and compliant with regulations.

Use case #4: Fraud detection and risk triage

In the traditional lending process, fraud detection and credit risk assessment are often treated as separate, sequential steps. AI enables a more integrated approach, evaluating both simultaneously in a single, holistic assessment at the point of application.

Modern models can cross-check submitted data against a wide range of signals in real time. This includes device fingerprints, IP addresses, and identity verification services, to flag inconsistencies that may indicate synthetic identity fraud. They can also detect anomalous transaction patterns that suggest account takeover or other malicious activity.

AI in credit scoring: Adoption roadmap

Adopting AI in credit scoring is far more than a technology upgrade—it represents a fundamental business transformation. Success requires more than simply procuring new tools; it demands a clear strategy, a phased implementation plan, and proactive management of organizational and regulatory challenges.

The specific path will vary depending on an institution’s size, resources, and existing infrastructure, so a one-size-fits-all approach is not going to work. Instead, executive leaders need a structured roadmap that guides the journey from initial planning to full-scale, optimized deployment.

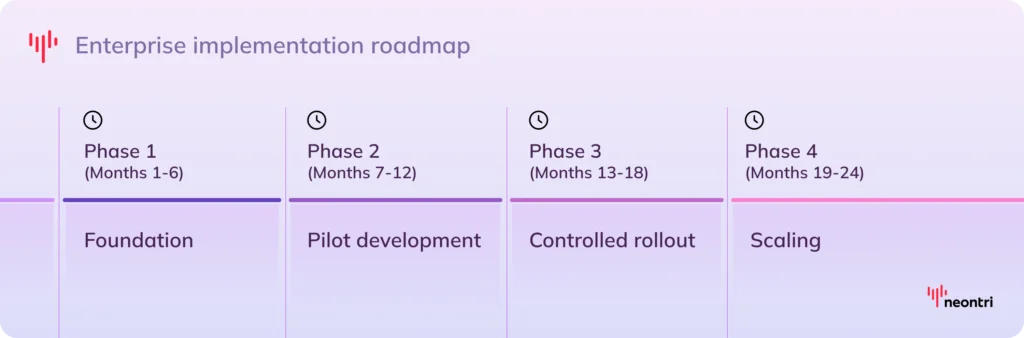

Enterprise implementation (12-24 month timeline)

Large financial institutions must balance tech innovation with stringent compliance regulations, legacy system integration, and organizational change. To manage this complexity, implementation is best approached through a phased process, ensuring that every stage builds on the last with minimal disruption and maximum business impact.

- Phase 1: Foundation (Months 1–6)

Begin with a comprehensive assessment of the institution’s existing data infrastructure to identify weaknesses in data quality, accessibility, and governance that could hinder AI adoption. The next priority is to establish a comprehensive compliance framework that aligns with both current regulations and anticipated future requirements, ensuring that innovation does not compromise regulatory trust. With this foundation in place, select a high-impact use case that offers clear business value as the pilot program.

- Phase 2: Pilot development (Months 7–12)

Develop and train the pilot AI model using real-world data to tailor it to the specific needs of the chosen use case. Integrate it into existing loan origination systems within a sandboxed environment, allowing for controlled experimentation without disrupting ongoing operations. Following this, conduct comprehensive testing covering performance, bias, and explainability to confirm that the model is both accurate and trustworthy.

- Phase 3: Controlled rollout (Months 13–18)

Introduce the model to a limited product line or a specific market segment. This cautious rollout provides a real-world test while containing potential risks. Continuous monitoring is crucial at this stage, as it captures feedback on accuracy, customer impact, and operational fit.

Additionally, start implementing staff training and structured change management programs to ensure that employees understand the new system and are ready to embrace it as part of their daily workflows. This helps build confidence across the organization.

- Phase 4: Scaling (Months 19–24)

The final phase brings the system into full production across all targeted products and business lines. By this point, the AI credit scoring model is mature enough to integrate seamlessly with broader digital transformation initiatives. The focus shifts toward refining performance, reducing operational costs, and unlocking additional value through advanced optimization.

Growth-stage implementation (6-12 month timeline)

Unlike large enterprises that may require multi-year rollouts, mid-sized lenders and fintechs often need to adopt AI-driven credit scoring quickly to stay competitive and capture new opportunities. Growth-stage implementation focuses on leveraging third-party vendor solutions, allowing institutions to accelerate deployment while minimizing the need for heavy in-house development.

- Phase 1: Rapid assessment (Months 1-2)

The first step is to quickly evaluate and select a trusted AI scoring solution provider. This involves comparing technical capabilities and integration potential to ensure the chosen partners can support both near-term goals and long-term scalability.

At the same time, assess internal data readiness to ensure seamless integration with the chosen solution. Where possible, an existing regulatory compliance framework can be adapted to streamline approval processes and avoid unnecessary delays. This concentrated effort sets the foundation for a fast and effective implementation.

- Phase 2: Implementation (Months 3–6)

Deploy the vendor’s solution is integrated into your system, focusing on tailoring workflows to reflect existing credit processes. Launch a pilot program with limited transaction volumes to test the system’s real-world performance, accuracy, and compliance. At the same time, conduct staff training and process development to ensure teams are equipped to work confidently with the new technology and integrate it into day-to-day operations.

- Phase 3: Production deployment (Months 7–12)

Begin using AI credit scoring at scale, expanding beyond the pilot program into broader lending operations. Gradually, the scope of implementation can be broadened to additional use cases, such as new products or customer segments. Work in collaboration with your vendor to ensure continuous optimization and fine-tuning, allowing the system to adapt as volumes increase and new data becomes available.

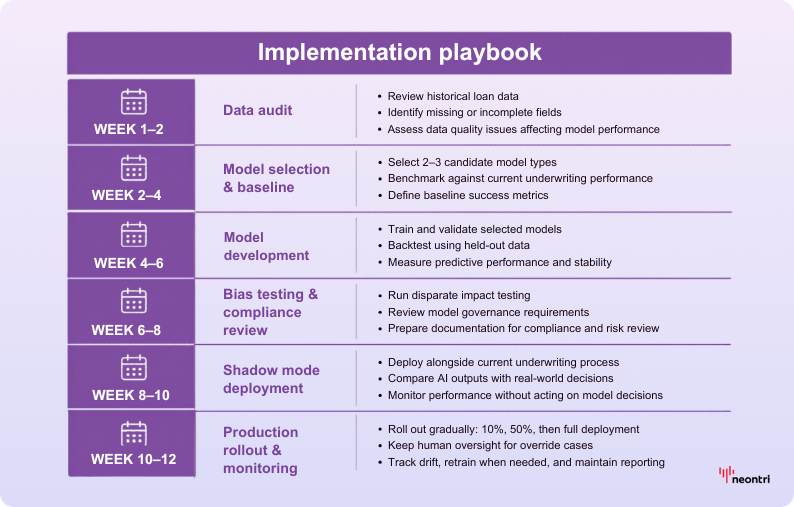

Implementation playbook: From data to production in 6–12 weeks

For institutions ready to move from planning to execution, the following playbook breaks down the critical first weeks of implementation into concrete, actionable steps.

- Week 1–2: Data audit

Review historical loan data to confirm what is available, what is missing, and what quality issues may affect performance. This stage also defines the main gaps that need to be addressed.

- Week 2–4: Model selection and baseline

Select two or three candidate model types from the options above and benchmark them against current underwriting performance.

- Week 4–6: Model development

Train, validate, and backtest the selected models using held-out data to measure predictive performance and stability.

- Week 6–8: Bias testing and compliance review

Run disparate impact testing and prepare the documentation required for model risk management, governance, and compliance review.

- Week 8–10: Shadow mode deployment

Deploy the AI model alongside current underwriting without acting on its decisions, then compare outputs and outcomes under real conditions.

- Week 10–12: Production rollout

Roll out gradually, starting with 10% of decisions, then 50%, then full deployment, with human oversight in place for override cases.

- Ongoing: Monitoring and retraining

Track model drift, retrain when needed, and maintain reporting to support performance, governance, and regulatory requirements.

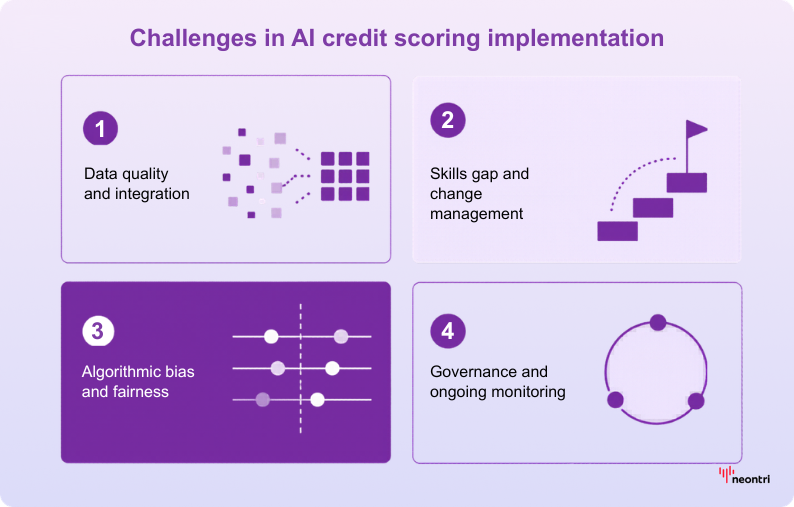

Confronting the challenges in AI credit scoring implementation

The implementation journey is not without its challenges. Proactively addressing these potential hurdles is key to a successful outcome.

- Data quality and integration

Integrating diverse and often messy data sources is a significant technical challenge. Enterprise solutions involve master data management platforms and API-first architecture, while growth-stage firms can leverage cloud-based platforms with pre-built connectors and third-party validation services.

- Skills gap and change management

The “skills gap” is often misunderstood as simply a shortage of data scientists. While technical talent is crucial, the broader challenge is fostering a data-literate culture across the entire organization.

A successful AI strategy requires more than a few PhDs in a back room; it requires credit officers who trust the model’s outputs, managers who understand its limitations, and executives who can align its use with business strategy. This necessitates a significant investment in broad-based education and upskilling.

A best-in-class example is BBVA’s “Data University,” an initiative that has engaged over 50,000 employees in data and AI training, demonstrating a commitment to organization-wide transformation, not just technological acquisition.

- Algorithmic bias and fairness

This is arguably the most critical and reputationally sensitive challenge. If not managed properly, AI models can inadvertently perpetuate or even amplify existing societal biases present in historical data, resulting in discriminatory outcomes known as “digital redlining.”

The Wells Fargo case serves as a powerful cautionary tale. In 2022, the bank faced serious allegations that its loan evaluation algorithm was producing discriminatory outcomes, assigning higher risk scores to Black and Latino applicants compared to white applicants with similar financial profiles.

This case highlights the absolute necessity of implementing robust bias detection and mitigation frameworks from the outset. This includes regular algorithmic audits, fairness testing, data debiasing techniques, and maintaining meaningful human oversight to prevent discriminatory results and ensure fair lending practices.

Regulatory compliance framework for AI credit scoring

The adoption of a technology as powerful as AI in a highly regulated field, such as credit scoring, inevitably brings intense scrutiny from regulatory bodies. The regulatory frameworks in the European Union and the United States, while different in their approach, converge on the core principles of risk management, transparency, and fairness. Fortunately, the same technological advancements that power AI scoring also provide the tools to meet these stringent compliance demands.

The EU AI Act: Mastering “high-risk” system governance

The European Union’s AI Act represents the world’s first comprehensive legal framework for artificial intelligence. Under this regulation, AI systems used for evaluating the creditworthiness of individuals or establishing credit scores are explicitly classified as “high-risk”. This designation triggers a specific and rigorous set of legal obligations that institutions must meet before and after deploying such systems.

Key requirements for high-risk AI systems under the EU AI Act include:

- Risk management systems: Institutions must establish, implement, and maintain a continuous risk management system throughout the entire lifecycle.

- Data governance: Strict frameworks for data governance and management are required, including data lineage tracking and assessments of data suitability to prevent biases.

- Technical documentation and transparency: Comprehensive technical documentation must be maintained, and systems must be designed to be transparent, allowing users to interpret the system’s output and use it appropriately.

- Human oversight: Effective human oversight must be in place, with clear measures to prevent or minimize risks.

- Post-market monitoring: A post-market surveillance system must be implemented to continuously monitor the AI system’s performance in a real-world environment and report any serious incidents.

Financial institutions operating in the EU should prepare now, as the current framework points to 2 August 2026 for the application of the high-risk AI rules.

US CFPB: The mandate for explainability

In the United States, the regulatory focus has been less on pre-market authorization and more on the outcomes of AI-driven decisions, particularly concerning fairness and consumer protection. The Consumer Financial Protection Bureau (CFPB) has made it unequivocally clear that existing laws, such as the Equal Credit Opportunity Act (ECOA) and its implementing Regulation B, apply with full force to AI credit scoring systems.

The central mandate from the CFPB is explainability. The bureau has explicitly stated that creditors cannot use “black-box” underwriting technology if it prevents them from providing the specific and accurate reasons for adverse actions (e.g., loan denials) as required by law. Generic, vague reason codes, such as “credit history” or “time at residence,” are deemed insufficient. Instead, the explanation must reflect the actual model inputs and their specific contribution to the negative decision, such as “a high number of recent credit inquiries” or “recent missed payments on existing obligations”.

Technical solutions for transparency: LIME, SHAP, and Auditable AI

The regulatory demand for explainability has spurred the development of powerful technical solutions that can peer inside the “black box” of complex machine learning models. Two of the most prominent and widely accepted techniques are LIME (Local Interpretable Model-agnostic Explanations) and SHAP (Shapley Additive exPlanations).

- LIME works by creating a simpler, interpretable local model around an individual prediction to explain how the complex system arrived at that specific decision.

- SHAP uses a game theory approach to assign a specific contribution value to each feature (e.g., income, debt-to-income ratio, recent payments) for every single prediction, showing precisely how much each factor pushed the score up or down.

These techniques provide the feature-level contribution analysis necessary to generate the specific, accurate, and regulatory-compliant adverse action notices required by the CFPB. By integrating these tools into their production systems, financial institutions can automate the generation of compliant explanations, turning what was once a major regulatory hurdle into a manageable, auditable process.

This dynamic reveals a crucial relationship between regulation and technology. The stringent legal requirements for transparency, particularly from the CFPB, have created a powerful market incentive for innovation in the field of explainable AI (XAI). Without this regulatory push, the industry might have remained content with more opaque, purely performance-driven models. This demonstrates that compliance and innovation are not opposing forces.

| Compliance area | EU AI Act | US (CFPB/ECOA/SR 11-7) | Recommended action |

|---|---|---|---|

| Risk management system | -Mandates a continuous, lifecycle-wide risk assessment and mitigation system. | -Requires robust model risk management, including independent validation and ongoing monitoring. | -Implement a formal model risk management (MRM) framework that explicitly covers AI/ML models. |

| Data governance | -Requires high-quality, relevant, and unbiased training data; mandates data lineage tracking. | -Governance over alternative data sources is critical to ensure fairness and prevent discrimination. | -Establish a centralized feature store with automated data quality monitoring and comprehensive lineage tracking. |

| Transparency & explainability | -Requires systems to be transparent, allowing users to interpret outputs. | -Mandates specific, accurate reasons for adverse actions. -“Black-box” models are not exempt. | -Integrate LIME and SHAP techniques into production systems to automate the generation of feature-level explanations for all credit decisions. |

| Human oversight | -Requires effective human oversight measures to be built into the system’s design and operation. | -While not explicitly mandated, human-in-the-loop governance is a best practice for managing model risk and handling complex cases. | -Develop clear escalation frameworks for human review of edge cases and high-risk decisions, with comprehensive logging of all overrides. |

| Post-market monitoring | -Mandates a post-market surveillance system to continuously monitor the AI system’s real-world performance. | -Requires continuous performance monitoring for model accuracy, stability, and fairness. | -Implement automated dashboards to track model performance, population drift, and fairness metrics in real-time. |

| Bias testing | -Requires regular testing for biases that could lead to discriminatory outcomes. | -A core component of fair lending compliance -Requires regular assessment of disparate impact across protected classes. | -Automate fairness testing across protected classes and their proxies. -Document all bias mitigation efforts and their outcomes. |

Additional compliance requirements institutions should plan for

Beyond the EU AI Act and CFPB explainability requirements, institutions also need a broader control framework that covers fair lending, model governance, privacy rights, and state-level AI obligations. In practice, this means treating AI credit scoring as a regulated operating capability, not just a model deployment project.

- Fair lending (ECOA / Regulation B)

US compliance depends on more than model accuracy. Institutions need regular disparate impact testing across protected classes, controls for proxy variables, and adverse action notices that reflect the actual reasons behind a credit decision rather than generic templates. This makes fair lending testing an ongoing requirement, not a one-time validation step.

- Model risk management (SR 11-7 / OCC guidance)

AI scoring models should sit inside a formal model risk management framework with clear ownership, independent validation, change control, performance monitoring, and documented limitations. For US-regulated banks, this governance model is anchored in SR 11-7 and OCC model risk guidance; the OCC updated that guidance in April 2026, but the core expectation remains the same: models must be controlled, validated, and auditable throughout their lifecycle.

- GDPR Article 22

In the EU, automated credit decisions also raise privacy-law obligations. Where a decision is based solely on automated processing and has legal or similarly significant effects, individuals have the right to obtain human intervention, express their point of view, and contest the decision. That means lenders need a clear human-review path, not just a technically sound model.

- CCPA and state-level AI rules

In California, CPPA regulations adopted in 2025 became effective on January 1, 2026, with phased compliance deadlines for some obligations beginning later. They include rules on automated decisionmaking technology, risk assessments, cybersecurity audits, and consumer rights around access and opt-out. In Colorado, the state’s high-risk AI law takes effect on June 30, 2026 and requires reasonable care to prevent algorithmic discrimination, along with notices, documentation, and impact-assessment style controls.

- Documentation requirements

Regulators will expect a complete audit trail. That should include model purpose, data lineage, feature lists, excluded-variable rationale, validation results, bias-testing evidence, adverse-action mappings, override logs, retraining history, and incident records. If these materials are incomplete, the governance framework will be seen as incomplete too.

How should institutions approach compliance when operating in both EU and US regulatory environments?

For organizations active in both the EU and the US, the most practical approach is to build a single compliance framework anchored to the EU AI Act. Its pre-market controls and full lifecycle governance are stricter than the US focus on outcomes such as fairness and explainability. So meeting EU standards covers nearly all CFPB and Regulation B requirements. A single system reduces duplication: one central feature store, a shared explanation engine (SHAP and LIME), and a unified audit trail can serve both regulators.

A typical phased plan includes:

- By early 2026, EU-compliant risk management and post-market monitoring are in place.

- By early 2027, CFPB-specific adverse-action reasons and disclosure templates are integrated into the explanation workflow.

- On an ongoing basis, a unified dashboard provides consolidated reporting on fairness metrics, model drift, and regulatory obligations in both jurisdictions.

This approach makes the EU’s 2 August 2026 high-risk AI milestone and ongoing US enforcement easier to manage.

The future of AI credit scoring

As financial institutions grapple with the current wave of AI adoption, the next frontier of intelligent credit is already taking shape. The evolution of this technology will continue to be driven by advancements in AI, a shifting landscape of risk and regulation, and the unceasing pressures of market competition. Executives must not only focus on present implementation but also maintain a strategic eye on the future to ensure long-term relevance and success.

Trend #1: Generative AI expands the credit toolkit

The rise of Generative AI, particularly large language models (LLMs), is set to significantly expand banks’ credit scoring capabilities beyond traditional predictive analytics. While traditional models specialize in scoring structured data, GenAI can interpret, summarize, and generate insights from vast amounts of unstructured information. In practice, this could mean:

- Enhanced credit analysis. Generative AI agents could autonomously review business loan applications, analyze financial statements, and draft initial sections of credit memos for human officers,accelerating underwriting for complex loans.

- Advanced portfolio monitoring. The systems could continuously monitor unstructured data sources like news articles, market reports, and regulatory filings to identify emerging risks for specific borrowers or entire industry segments.

Trend #2: Regulation grows more complex

As AI becomes more embedded in credit decisioning, regulators are sharpening their focus on fairness, transparency, and accountability. Models will need to withstand scrutiny not just for accuracy, but for explainability and resilience against bias. Institutions that proactively invest in compliance-ready frameworks will be better positioned to scale responsibly and maintain trust.

Trend #3: Competition intensifies

The divide between early adopters and slower movers is likely to widen. Institutions already experimenting with next-generation AI will enjoy a compounding advantage—faster decision-making, deeper insights, and stronger customer relationships. Those who delay may find the barriers to catching up increasingly steep, especially as technology becomes more deeply integrated into risk management and customer engagement strategies.

Best practices for AI credit scoring implementation

Building a successful AI credit scoring program demands a disciplined commitment to best practices that cut across data, governance, ethics, and leadership strategy. Institutions that approach implementation holistically—treating it as both a technical and organizational transformation—will be best positioned to capture long-term value. The following recommendations provide a framework for executive leaders on how to achieve that:

Develop a robust data strategy. High-quality, well-governed data is the lifeblood of any AI system. For large enterprises, this means investing in centralized feature stores, automated data quality monitoring, and robust data lineage tracking from source to decision. For growth-stage institutions, success often comes from forming strategic partnerships with data aggregators while implementing consent management systems that align with regulations like GDPR and CCPA.

Here’s how to aggregate, clean, and validate alternative data the right way:

- Set clear governance and quality standards.

- Automate cleaning and validation to catch and remove errors.

- Use a centralized data catalog or feature store for consistency.

- Partner with trusted providers and document compliance.

- Pilot new data sources to check accuracy and bias before scaling.

- Maintain end-to-end data lineage for accountability.

Establish rigorous model governance. Strong model governance is essential to maintaining both performance and trust. Institutions should adopt a “champion-challenger” framework, where new models (challengers) are continuously tested against the production model (champion). This ensures that only the most effective approaches remain in use while driving ongoing performance improvements.

Commit to a data-first culture. Successful AI implementation is fundamentally an organizational transformation. Beyond infrastructure, leadership must foster broad-based data literacy programs to upskill the entire organization, ensuring teams across the organization understand, trust, and effectively use AI-driven insights.

Turn strategy into execution

Move AI credit scoring from framework to execution with expert support across data strategy, model development, governance, and production deployment.

Prioritize a lifecycle-wide strategy. AI credit scoring should not be viewed as a single-point solution for loan origination. Organizations should develop a holistic strategy that leverages AI across the entire credit lifecycle—from underwriting and portfolio monitoring to collections and fraud detection. By embedding AI at each stage, institutions can maximize ROI while building a sustainable competitive edge. This lifecycle approach also enables a continuous flow of insights, creating a feedback loop that strengthens both customer relationships and risk management.

Mitigate bias. Managing algorithmic bias is both a regulatory obligation and an ethical imperative. Continuous fairness testing should be automated to monitor for disparate impacts in approval rates and pricing across protected groups. When potential issues are identified, institutions must have predefined remediation processes in place—whether that means adjusting existing models or building alternative versions that minimize bias while preserving predictive accuracy. By incorporating fairness into a systematic model management approach, institutions can mitigate reputational risk while promoting more inclusive lending practices.

Adopt a phased implementation. AI implementation is most effective when it starts small and scales fast. A well-defined pilot program focused on a high-impact use case allows institutions to demonstrate tangible ROI quickly, while minimizing risk. The insights and momentum generated from this first phase can then be leveraged to secure organizational buy-in and support a broader rollout across multiple product lines and functions.

Act with urgency. The pace of change in financial services leaves little room for hesitation. Institutions that adopt a “wait-and-see” approach risk falling behind irreversibly. Executive teams must therefore treat intelligent credit not as an optional experiment but as a strategic imperative—and act decisively to capture first-mover advantages.

What are the best practices for integrating AI credit scoring with existing legacy systems?

Institutions achieve reliable integration by treating legacy systems as data sources and adding AI in controlled, secure steps. The following core practices ensure success:

- Connect legacy systems to a central feature store using APIs or ETL pipelines.

- Run nightly batch updates for logs and real-time streams for live AI decisions.

- Start in shadow mode and scale to 5–10 % of one product after validation.

- Monitor accuracy, drift, and fairness in production with automated alerts.

- Keep an instant fallback to legacy rules via a kill switch.

- Secure the pipeline with encryption, access control, and PII minimization.

- Align with model risk management through independent validation and audit logs.

This structured path delivers full integration in 12–18 months with low risk and strong compliance.

Transform AI ideas into real-world solutions with Neontri

At Neontri, we support financial and banking institutions in moving AI initiatives from strategy to tangible business results. Our Gen AI service offerings span strategic planning, data readiness, model development and deployment, and continuous optimization and governance.

Neontri’s lending innovation project: AI-powered decisioning for loan and credit providers

Challenge: Loan and credit providers needed a more efficient way to manage complex lending workflows. Manual steps and fragmented logic made it harder to scale decisions, adapt to change, and control costs.

Approach: Neontri developed an AI-powered decisioning engine for the fintech sector that automated complex workflows and gave teams more control over decision logic and lending rules.

Results:

- 78% lower engineering costs for new features

- 80% decrease in ongoing post-launch support costs

- 51% reduction in infrastructure spend through cloud architecture optimization

- Reduced the operational burden on business teams by removing IT tasks from their daily workload

Why it matters: This project shows how AI can improve lending operations through stronger workflow control, scalability, and measurable cost savings.

Contact us to move from concept to implementation with confidence—and turn your vision for intelligent credit into a scalable, real-world solution.

Final thoughts

The rise of intelligent credit scoring marks a decisive inflection point for the financial industry. Organizations that successfully align advanced AI capabilities with sound governance and ethical safeguards will transform lending decisions from a backward-looking measure of risk into a catalyst for sustainable growth. By anticipating future borrower behavior rather than merely assessing past performance, they can unlock new opportunities, personalize loan products at scale, and extend responsible lending to previously underserved markets.

The organizations that act now will shape the future of credit itself—setting new standards for accuracy, fairness, and inclusion in the era of intelligent finance. The path forward is clear: build the frameworks, deploy the technology, and claim your place at the forefront of intelligent finance.

FAQ

Can credit scoring with AI improve approval rates without increasing default risk?

Yes. By using a broader range of data to achieve more accurate predictions of default risk, AI models can more effectively distinguish between high-risk and creditworthy applicants within traditionally “risky” segments. This allows institutions to safely approve a greater number of qualified borrowers who would have been rejected by legacy systems, thereby increasing approval rates without a corresponding increase in the portfolio’s overall default rate.

How does AI improve the accuracy of credit scoring?

AI improves accuracy in two main ways. First, it ingests and analyzes a much larger and more diverse set of data, including real-time and alternative data, such as bank transactions and utility payments, to create a more holistic view of a borrower’s financial health. Second, its machine learning algorithms are capable of identifying complex, non-linear patterns and subtle correlations between thousands of variables—relationships that are invisible to the simpler, linear models used in traditional scoring. This combination of richer data and more powerful analytics leads to more precise, individual-level risk predictions.

How quickly can an AI credit scoring system be implemented in an existing lending process?

The implementation timeline depends on the institution’s size and approach. For growth-stage institutions or those leveraging third-party, cloud-based solutions, a phased implementation can be achieved in 6-12 months. For large enterprise institutions building bespoke, deeply integrated systems, a more comprehensive timeline of 12-24 months is realistic, encompassing foundational data infrastructure work, pilot development, a controlled rollout, and full-scale optimization.

How does AI credit scoring integrate with existing core banking or loan origination systems?

Modern AI credit scoring solutions are designed for integration. They typically use an API-first architecture, allowing them to seamlessly connect with existing Loan Origination Systems (LOS) and core banking platforms. The AI system functions as an intelligent decision engine; the LOS can send an application data packet to the AI model via an API call and receive a score, a decision recommendation, and a compliant explanation packet back in real-time, which is then used to continue the workflow within the existing system.

How transparent are AI credit scoring decisions for customers and regulators?

Modern AI systems are designed to be highly transparent, moving away from the “black-box” reputation of early models. For regulators and internal auditors, techniques such as LIME and SHAP provide a clear, auditable trail that shows exactly which data features contributed to any given decision and by how much. For customers who are denied credit, these same techniques automatically generate the specific, plain-language reasons required for adverse action notices under ECOA, ensuring that the decision-making process is both compliant and understandable.

How can banks ensure their AI credit scoring systems remain adaptable to evolving regulations and market conditions?

Banks can keep their AI credit scoring systems flexible by tracking accuracy, bias, and drift, and by updating models regularly with clear version control. They should ensure compliance with current regulations, use explainable AI to maintain transparency, and integrate risk management frameworks. Starting with pilot programs and scaling gradually while involving compliance, data science, and risk teams helps banks adjust quickly to market and regulatory changes.

How much can AI reduce default rates in credit scoring?

Financial institutions report default rate reductions of 25–30% after switching to AI-based credit scoring. This improvement comes from analyzing a broader dataset that identifies risk signals legacy systems miss, combined with continuous learning that adapts to emerging patterns in real time. In one documented case, a UK high street bank identified 83% of bad debt that traditional scores had missed entirely. The exact reduction depends on portfolio composition, data quality, and how comprehensively alternative data is integrated.

Is AI credit scoring compliant with fair lending laws?

Yes, when properly implemented. AI models must comply with ECOA and Regulation B in the US, and the EU AI Act in Europe. The critical requirement is disparate impact testing. Institutions must prove their model doesn’t produce adverse outcomes for protected classes, even indirectly through proxy variables like zip code or spending patterns. Compliance requires ongoing bias monitoring, explainability tools like SHAP, and adverse action notices that reflect actual model inputs rather than generic reason codes.

How long does it take to deploy an AI credit scoring model?

Deployment timelines vary by institution size and implementation model. Growth-stage lenders using third-party cloud solutions can often reach production in 6 to 12 months, while large institutions building bespoke systems integrated with core banking infrastructure typically require 12 to 24 months. In most cases, the biggest delays come from legacy system integration and data quality remediation, not from model development itself.

What’s the difference between AI credit scoring and traditional FICO-based scoring?

FICO uses a fixed formula applied to a limited set of bureau variables (payment history, utilization, credit age). It produces a static snapshot that requires manual updates to change. AI credit scoring analyzes thousands of variables simultaneously, including real-time transactions and alternative data, producing dynamic individual-level risk profiles. The practical result is 15–25% better default prediction accuracy and the ability to assess thin-file borrowers that FICO simply can’t score.

Can AI credit scoring use alternative data? What about compliance?

Yes, and alternative data is one of AI scoring’s primary advantages. Bank transactions, utility payments, rent history, and cash flow patterns help assess borrowers invisible to traditional bureau data. The compliance requirement is that all alternative data sources must be tested for disparate impact before deployment, since proxy variables can create indirect discrimination. Consent management must also align with GDPR in the EU and CCPA in California. Properly governed alternative data improves both accuracy and financial inclusion.

How much does it cost to build an AI credit scoring system?

A full bespoke enterprise build typically ranges from $2–5M over 18–24 months. Growth-stage institutions using vendor solutions can implement for $200K–800K depending on integration complexity. Ongoing costs include model monitoring, retraining, and compliance documentation. The more useful frame for most executives is ROI: institutions report operational cost reductions of up to 22% and default rate reductions that generate millions in avoided charge-offs annually, making the investment case straightforward to build.

Do we need to replace our current underwriting system to add AI?

No. AI credit scoring integrates with existing loan origination systems via API. The model functions as a decision engine alongside current infrastructure – your system sends application data, receives a score and compliant explanation in return, then continues its normal workflow. The recommended approach is to start in shadow mode alongside existing underwriting, validate performance, then scale gradually. Replacing existing infrastructure is neither necessary nor advisable as a starting point.

How do we handle the EU AI Act for credit scoring in 2026?

Credit scoring falls under the EU AI Act’s high-risk category, making 2026 the key window for readiness. Institutions need a conformity assessment, continuous bias testing, human oversight with override controls, and audit-ready technical documentation. For banks operating across both the EU and the US, one framework built to EU standards can also cover most CFPB requirements.

Build vs. buy: When should a bank build its own AI credit scoring model?

Building makes sense when proprietary data creates a real advantage, the risk profile is highly specific, or underwriting is a strategic differentiator. Buying is usually the better option when speed, lower implementation risk, and faster deployment matter most. For many mid-sized institutions, a hybrid approach works best: vendor solutions for standard products and custom models for strategic segments.

How do we explain AI credit decisions to customers and regulators?

Explainability works at two levels. For regulators, SHAP and LIME provide a feature-level audit trail showing exactly which variables drove each decision, satisfying SR 11-7 and EU AI Act documentation requirements. For customers receiving adverse action notices, the same tools generate specific plain-language reasons required under ECOA: not “credit history” but “high number of recent credit inquiries.” Both outputs can be automated and integrated directly into existing loan origination workflows.