As banks and fintech companies continue to innovate and enhance their mobile offerings, the appeal of banking apps is set to grow even further. This article covers the full picture: what mobile banking technology is and the benefits it brings, the adoption data defining the market, the core technology stack powering today’s leading apps, and the trends that will determine the future of this rapidly evolving sector.

What is mobile banking technology?

Mobile banking technology refers to the underlying infrastructure, software, application programming interfaces (APIs), artificial intelligence models, and integrated services that allow users to access and manage their finances via smartphones, tablets, or wearable devices.

Once restricted to balance checks and transfers, modern mobile banking technology has evolved into a fully integrated digital ecosystem. On the frontend, it delivers native cross-platform interfaces featuring biometric security, real-time transaction processing, and conversational AI assistants that act as active financial advisors. On the backend, it connects directly to cloud-native microservices, open banking frameworks, embedded finance APIs, and instant payment rails.

What distinguishes mobile banking technology in 2026 from what came before is a fundamental shift from a reactive utility to a proactive financial companion. There are several core architectural and operational innovations that distinguish modern mobile banking applications:

- Predictive insights. Previous mobile banking tech showed you what was already spent. Today’s technology uses localized, on-device machine learning models to analyze cash flow patterns, automatically forecast upcoming expenses, identify forgotten subscriptions, and prompt users to move excess cash into yield-bearing accounts before they even think to do so.

- Zero-trust security. Mobile banking has abandoned vulnerable password-and-SMS authentication models and instead relies on decentralized identity frameworks and passkeys, leveraging secure enclaves on users’ devices.

- Cross-ecosystem embedding. Financial services are no longer confined to the bank’s proprietary app. Through advanced API-first design, mobile banking technology allows users to securely authorize payments, check credit limits, or split bills directly inside third-party platforms, whether they are shopping in an e-commerce marketplace, splitting a rideshare fare, or authorizing a payment through a smart home hub.

Mobile banking adoption: The shift to digital-first finance

Industry reports show that mobile has become the dominant channel for financial management across every major market. Driven by demand for 24/7 convenience and friction-free account management, consumers are increasingly replacing traditional branch interactions with mobile banking apps. This shift is reflected in the latest industry statistics, which highlight the rapid growth of mobile adoption and the increasingly central role this technology plays in everyday life.

- The global mobile banking market is projected to expand from $1.87 trillion in 2025 to $6.42 trillion by 2033, as smartphones become the primary gateway for global financial inclusion and real-time banking services. (Fortune Business Insights, 2026)

- Mobile banking has reached 2.3 billion registered accounts globally, though only 25.7% of those are active on a monthly basis, indicating a significant engagement gap that institutions are racing to close. (GSMA, 2026)

- 53% of banking clients log in to their primary financial app daily: 31% once a day, and 22% multiple times a day. Millennials are the heaviest daily users, with 40% logging in daily and 31% more often. Gen Z spreads engagement more evenly: 32% check in a few times per week, while only 26% maintain consistent daily habits. Gen X and Baby Boomers sit closer to the mean, at 50% and 41% daily-or-more, respectively. (MX Technologies, 2025)

- The average consumer now juggles three or more finance-related mobile apps on their phone. This fragmented usage has triggered an era of app consolidation, with 57% of users stating they would prefer to link all of their accounts into a single, unified mobile application if given the option. (MX Technologies, 2025)

- 74% of consumers express a desire for more personalized banking experiences. 66% Gen Z want their provider to actively use their data to tailor their experience. Among Millennials, 68% expect their institution to know them as individuals, and 64% are prepared to share more data if it yields a better outcome. (Q2, 2025)

- 60% of digital banking Americans say it is important for their data to be used to make relevant product recommendations, and those who are completely satisfied with how that data is used are 42% more likely to be loyal to their provider, 42% more likely to recommend it to family and friends, and 38% more likely to engage with additional digital products and features. (Alkami, 2025)

Mobile banking technology advantages across the financial ecosystem

Mobile banking’s rise is not simply a story of convenience – it reflects a fundamental realignment of value for every party in the financial relationship. For consumers, it removes the friction that once defined banking: no queues, no branch hours, no paperwork delays. For institutions, it compresses the cost of service delivery while opening new channels for engagement, data, and revenue.

The sections below examine what mobile banking technology delivers from both the customer’s and the bank’s perspectives.

Benefits of mobile banking for clients

Smartphones have become the primary gateway to digital banking for billions worldwide. As financial brands compete to deliver superior mobile experiences, innovation in this space continues to accelerate. Here are the top 12 reasons mobile banking remains so popular among customers.

- Mobile banking anytime. Modern mobile banking solutions allow customers to check their account balance or transaction history anytime, anywhere. Thanks to the analytical features in apps, users can easily track their expenses and know exactly how much they spend on food, entertainment, trips, etc. Additionally, they often provide personalized financial insights and budgeting tools to help customers better manage their finances and achieve their savings goals.

- Paying bills on time. Mobile banking applications help users stay on top of bill payments by sending timely reminders about upcoming due dates and enabling automatic or recurring payment setups, reducing the risk of missed deadlines and late fees.

- Financial awareness. Using mobile banking apps leads to a better understanding of financial products and services. Features like spending trackers and budgeting tools help users take control of their finances. And the more informed they feel, the more confidently they engage with their bank’s products.

- Accessibility. Mobile banking expands financial services for people previously left out of the traditional system. With just a smartphone and an internet connection, users in remote areas or with limited mobility can set up accounts, send money, or apply for a loan. No branch is required.

- Faster problem resolution. When something goes wrong, mobile banking puts the solution directly in the user’s hands. A lost card can be frozen in seconds with a single tap, and in-app chat connects users to support with full transaction context already loaded. There’s no need to repeat information or wait on hold.

Benefits of mobile banking for financial institutions

By embracing mobile-first solutions, banks optimize operations, enhance customer satisfaction, and position themselves for long-term growth in an increasingly digital economy.

- Better understanding of customer behavior. Mobile banking platforms generate a continuous stream of behavioral data, from spending habits and usage patterns to engagement metrics. Banks that use this data effectively can offer more relevant financial products, sharpen risk assessment, and make marketing efforts far more precise.

- Real-time customer interaction. Mobile applications enable banks to maintain consistent, real-time communication with users through push notifications, personalized messages, and in-app interactions. This ongoing digital connection fosters higher engagement, as customers are more likely to interact with services when they are easily accessible.

- Faster innovation. Mobile platforms allow banks to roll out new features, test updates, and refine services much faster than traditional infrastructure. This agility delivers a competitive edge by responding swiftly to market trends, customer feedback, and emerging technologies, without past delays.

- Security and fraud prevention. Mobile banking provides banks with a continuous stream of security signals (device data, location, biometrics, and behavioral patterns), making it far easier to detect suspicious activity quickly and accurately. Risk is assessed throughout the entire session, not just at the moment of a transaction, so threats are identified earlier. When the system flags unusual activity, the bank can act immediately by blocking the account, notifying the user, and resolving the issue in minutes rather than days.

- Deeper customer retention. Mobile banking helps banks retain customers by becoming part of their daily routines. Features such as balance checks, budgeting tools, and automated savings make the app consistently useful, increasing convenience and reducing the appeal of switching. Banks that provide meaningful everyday value are more likely to build long-term customer loyalty.

Lead the mobile banking revolution

Start your journey with us

Core mobile banking technology stack: Building the engine of digital banking platforms

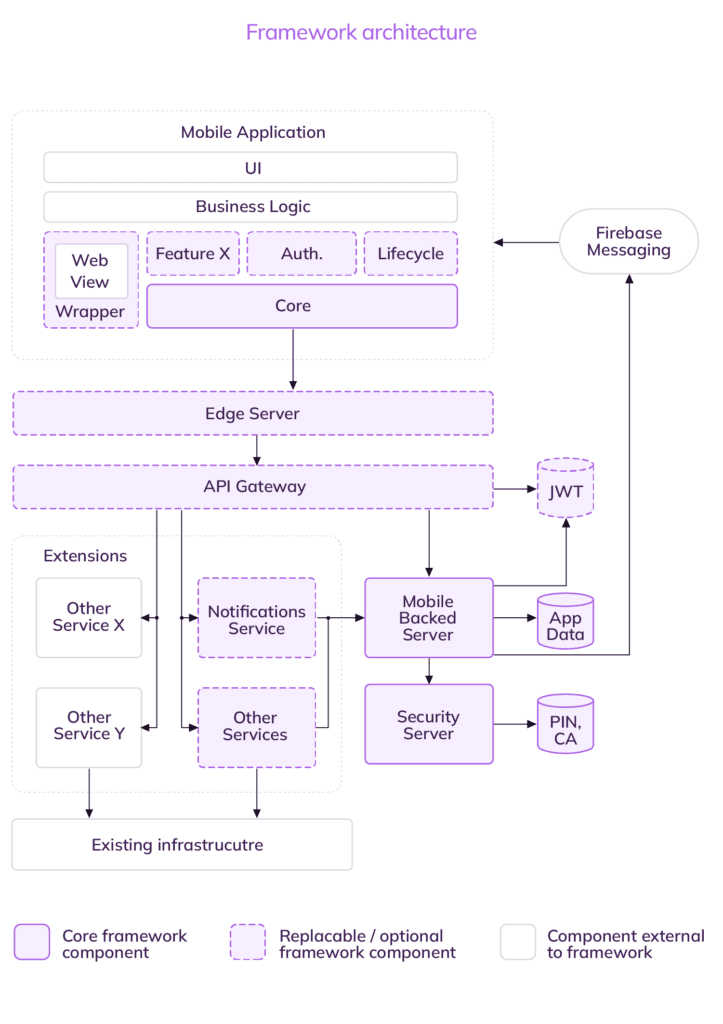

Modern mobile banking does not run on a single system. It is a layered architecture where each component handles a distinct function, and the quality of the overall experience depends on how cleanly those layers connect.

- Client layer

The client layer is the user-facing component of the mobile banking ecosystem, responsible for delivering a fast, intuitive, and secure customer experience. It is typically developed using native technologies such as Swift for iOS and Kotlin for Android to maximize performance and access on-device hardware. This layer handles interface rendering, transaction displays, local data storage, push notifications, and device-level capabilities such as biometric authentication, camera access, and digital wallet integration.

- Authentication layer

The authentication layer serves as the primary security gateway for the mobile banking application, verifying user identities and controlling access to sensitive financial services. To balance strong security with a seamless user experience, modern banking apps increasingly rely on passwordless authentication standards such as FIDO2, combined with multi-factor authentication (MFA) and device-based security controls.

In regulated markets, this layer must also comply with requirements such as PSD2 Strong Customer Authentication (SCA), which mandates the use of multiple independent verification factors. To meet these standards, the authentication system establishes a secure link between the customer’s identity, their trusted device, and the specific transaction being authorized, using biometric technologies such as fingerprint and facial recognition.

- Middleware layer

The middleware layer serves as the communication bridge between the mobile application and the bank’s backend systems. Acting as a central traffic controller, this layer, typically presented by an API gateway, provides a single, secure entry point for all client queries, ensuring that data flows efficiently between users and the services they need.

This layer is responsible for routing requests to the appropriate backend systems, validating authentication tokens, enforcing security policies, managing API versions, handling protocol translation, and applying rate limits to prevent abuse. It also orchestrates interactions across multiple services, enabling mobile applications to retrieve account information, process payments, connect to third-party providers, and deliver real-time functionality without exposing core banking systems directly to external networks.

- Core banking integration layer

This is the engine room of the mobile banking architecture, where actual ledger balances, transaction histories, and account records are processed and maintained. It ensures that core activities, including balance updates, fund transfers, and card transactions, remain synchronized across all channels.

In most financial institutions, this layer operates within a hybrid environment. A modern integration framework typically sits in front of legacy systems, abstracting their constraints from the customer-facing products. This decoupling allows banks to modernize digital experiences without requiring a full replacement of core infrastructure.

- Analytics layer

Operating silently in the background, this layer continuously monitors user behavior, transaction flows, and system activity to detect suspicious patterns and emerging threats in real time. By combining machine learning models, rules-based engines, and real-time risk scoring, it can identify unusual account access, flag potentially fraudulent transactions, and trigger step-up authentication when necessary.

Beyond its security function, the same infrastructure supports advanced data analytics capabilities. Streaming and batch data pipelines ingest behavioral signals to optimize application performance and refine personalization systems. As a result, this layer not only strengthens fraud prevention but also generates valuable customer insights that power personalization, targeted product recommendations, customer segmentation, and broader business intelligence initiatives.

A practical way to understand how these layers operate in production is to view them as a coordinated system rather than isolated components. When a user performs an action in a mobile banking app, that single interaction flows through all architectural layers, from the interface down to core systems and back, each layer performing a specific role in delivering a secure, real-time response.

A strong example of this tiered architecture can be seen in the mobile banking application IKO, developed by Neontri for PKO Bank Polski. In this system, a single user action traverses all layers seamlessly.

At the client layer, the app provides an intuitive, high-performance interface where users initiate actions and receive real-time feedback. The request then passes through the authentication layer, where identity is verified using secure authentication methods before any sensitive operation is allowed. Next, the middleware and API gateway layer routes the interaction through secure channels, ensuring proper validation and service orchestration. The core banking integration layer then processes the actual financial operation by interacting with ledger systems and updating account states within the bank’s infrastructure.

Build vs. buy: Implementing mobile banking technology

Understanding how mobile banking works is only part of the challenge. The next question for banks, credit unions, and fintechs is how to translate that vision into a production-ready digital banking platform. Whether launching a new mobile experience or modernizing an existing one, institutions must decide between building capabilities in-house, purchasing a pre-built platform, or adopting a hybrid approach.

Building a mobile banking solution from scratch provides maximum flexibility and control. Institutions can tailor the user experience, integrate proprietary services, and create differentiated features that align with their long-term digital strategy. However, this approach requires significant investment in engineering talent, security, compliance, infrastructure, and ongoing maintenance.

Building from scratch offers maximum control over architecture, security design, and feature roadmap. However, this approach requires significant investment in engineering talent, infrastructure, compliance, and ongoing maintenance. A greenfield native build typically spans 12 to 24 months before a production-ready release, or even longer if legacy core systems require custom integration work.

Buying a pre-built platform or leveraging Banking-as-a-Service providers accelerates time-to-market and reduces the complexity of mobile banking app development. For institutions entering new markets or operating under tight timelines, this approach converts an engineering problem into a configuration and integration problem. The trade-off, however, is a loss of absolute customization, meaning institutions must balance the speed of a ready-made framework against the long-term limits it may place on feature development.

Increasingly, financial institutions are turning toward a hybrid deployment model. Core banking and compliance functions may be sourced from established providers, while customer-facing experiences, AI-driven personalization, and differentiating features are developed internally. This approach captures the speed and cost-efficiencies of third-party vendors while preserving the creative control needed to innovate and minimize implementation risk.

Top mobile banking trends to watch in 2026 and beyond

The mobile banking technology landscape is undergoing a paradigm shift. Moving beyond basic transaction utility, the next generation of digital banking is being defined by autonomous execution, hyper-personalization, stronger regulatory alignment, and deeper infrastructure resilience. Together, these forces are reshaping how financial services are delivered and experienced. Below are six dominant trends driving this evolution.

Trend #1: Agentic AI for proactive banking

Agentic AI moves beyond chatbots into autonomous systems that can plan, reason, and execute multi-step tasks without constant user input. Instead of simply displaying spending summaries or alerts, these AI agents can initiate payments, optimizing savings allocations based on goals and risk tolerance, scan market rates and respond to changes in real time, or negotiate lower subscription bills. The result is a shift from reactive banking tools to proactive financial assistants that operate almost like a personal financial manager embedded within the app.

Trend #2: AI-driven personalization

Driven by advanced machine learning, mobile personalization has evolved from static product suggestions into context-aware financial coaching embedded directly within the app interface. Instead of simply looking back on past behavior, these AI systems analyze real-time spending habits, anticipate upcoming cash-flow patterns, and offer proactive guidance precisely aligned with a user’s current goals.

Rather than treating the user to post-spending alerts, these tools act as interactive financial partners. They can predict potential shortfalls days before they happen, suggest immediate savings adjustments, and recommend timely financial choices based on a user’s real-life context. Ultimately, this transforms the mobile interface from a passive, rear-view dashboard into an interactive financial tool that helps customers make optimal decisions in the moment.

Trend #3: Embedded finance

Banking-as-a-Service (BaaS) and embedded finance APIs allow everyday consumer brands to plug financial products directly into their customer journeys. Instead of redirecting customers to a bank, non-financial platforms are becoming all-in-one destinations, enabling users to buy insurance inside a travel checkout, access instant buy-now-pay-later (BNPL) micro-loans at a retail register, or track merchant loyalty points right alongside their purchases.

This cross-industry absorption is forcing traditional banks to rewrite their corporate strategies to avoid losing direct access to consumers. More than half of the top ten firms are actively planning to incorporate their native functionality within retail, healthcare, and other industry environments. Among these institutions, 27% believe this integration will occur by the end of 2030, while 67% expect it to take hold after 2030.

Trend #4: Account-to-account payments

Instant, account-to-account (A2A) payment rails are increasingly displacing traditional card networks across a growing share of mobile transactions. Integrated directly into mobile banking applications, A2A infrastructure enables users to bypass legacy intermediaries entirely and route funds immediately from one bank account to another.

For consumers, this creates a frictionless checkout experience, in which transfers are initiated via biometrically authenticated QR codes or deep-linked payment requests and settle within milliseconds. For merchants, dropping traditional card rails eliminates costly interchange fees, directly improves profit margins, and simplifies cash flow management.

Powered by Open Banking frameworks and state-backed real-time clearing networks, A2A transactions have rapidly evolved from a niche alternative into a dominant global payment mechanism. A report by Jupiner Research forecasts that the total transaction value of global A2A payments will surge by 113% over the next five years, climbing from $91.5 trillion to $195 trillion. This massive trajectory underscores a permanent, structural shift toward real-time payment ecosystems worldwide.

Trend #5: Quantum-safe cryptography readiness

As quantum computing continues to advance, it poses a long-term but fundamental threat to the cryptographic foundations that secure modern digital banking. Widely used public-key algorithms such as RSA and elliptic curve cryptography (ECC), which underpin authentication, data encryption, and secure communications, are expected to become vulnerable once sufficiently powerful quantum systems emerge.

In response, forward-looking financial institutions are beginning the gradual transition toward post-quantum cryptography (PQC). Apart from future risk, this move is also friven by the harvest-now, decrypt-later threat model, where adversaries collect encrypted banking data today to decrypt it once quantum capabilities mature. That’s why core security components such as authentication protocols, API encryption layers, and exchange mechanisms must be upgraded or replaced to remain secure in a post-quantum environment.

Trend #6: ESG features in apps

Environmental, Social, and Governance (ESG) considerations are increasingly moving beyond corporate disclosures and into the day-to-day banking experience. Driven by both regulatory requirements and growing consumer demand for sustainable financial products, banks are integrating ESG-focused features directly into their mobile applications.

Modern banking apps now allow customers to apply for green loans, invest in sustainability-focused funds, choose eco-friendly payment cards, and monitor the environmental impact of their spending. Carbon footprint calculators, for example, can estimate emissions associated with purchases and provide insights into how spending habits compare with sustainability goals.

For financial institutions, these capabilities serve a dual purpose. They help meet evolving ESG reporting and transparency requirements while also strengthening customer engagement by aligning financial services with personal values.

Conclusion

With all the possibilities and benefits of mobile banking apps, the future of this technology looks incredibly promising. As user expectations continue to evolve, banks and fintech providers must stay ahead by delivering seamless, secure, and feature-rich mobile experiences. The ongoing integration of AI, biometrics, and personalized financial tools will only enhance the value mobile apps bring to both consumers and institutions.

FAQ

What is mobile banking technology?

Mobile banking technology is the digital infrastructure, software, and protocols that allow customers to conduct financial transactions remotely using mobile devices like smartphones or tablets. It combines mobile apps, secure backend infrastructure, APIs, and core banking systems to deliver real-time self-service banking capabilities outside traditional branches.

How does mobile banking work technically?

Mobile banking operates on a client-server architecture, in which the mobile app (the client) communicates with the bank’s centralized core systems (the server) through secure APIs. When a user initiates an action, like a money transfer, the app sends an encrypted request over the internet using secure communication protocols. The bank’s backend servers validate their identity, check the database to ensure funds are available, execute the database transaction, and send an encrypted confirmation back to the app in real time.

What are the latest trends in mobile banking?

The latest trends are dominated by generative AI and the rise of super apps that bundle banking with services like travel booking, insurance, and digital ID verification. Hyper-personalized AI assistants are shifting apps from basic transactional tools into predictive financial advisors that can automate savings and anticipate major life events. Additionally, there is a massive push toward embedded finance, in which banking features are integrated directly into non-financial retail and gig-economy platforms, alongside the rapid implementation of real-time payment rails.

What technologies make mobile banking secure?

Mobile banking security relies on a multi-layered defense system, beginning with end-to-end encryption protocols that protect data in transit by rendering it unreadable to unauthorized parties. On the device itself, hardware-backed biometric authentication, such as Face ID or Touch ID, ensures that access is granted only to the verified user, eliminating reliance on easily compromised static credentials.

On the backend, banks deploy advanced machine learning algorithms and behavioral analytics to continuously monitor transactions and user activity in real time. These systems build dynamic risk profiles, detect deviations from normal behavior, and immediately flag anomalies or spoofing attempts, enabling rapid intervention to prevent fraud before it escalates.

How do banks build a mobile banking app?

Building a mobile banking app involves a rigorous software development lifecycle tailored to meet stringent security and compliance standards. Software engineers typically use cross-platform frameworks to build a smooth frontend user interface. This frontend is then integrated via secure API gateways to the bank’s core banking systems and cloud infrastructure, followed by months of exhaustive penetration testing and regulatory compliance audits to guarantee data privacy.

What’s the difference between mobile banking and online banking?

Online banking refers to accessing financial services through a web browser on a desktop or laptop. Mobile banking, by contrast, is delivered through a dedicated app on a smartphone or tablet, leveraging built-in device capabilities, including biometric authentication, push notifications, NFC payments, GPS for finding nearby ATMs, and camera-based document scanning.

Sources

https://www.fortunebusinessinsights.com/mobile-banking-market-114735

https://hub.q2.com/resources/col/pf/2025-retail-banking-trends-and-priorities-report

https://kpmg.com/xx/en/what-we-do/services/ai/intelligent-banking.html

https://www.mx.com/research/gen-z

https://www.mx.com/research/millenials

https://www.mx.com/research/gen-x

https://www.mx.com/research/baby-boomers

https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/gsma_resources/the-state-of-the-industry-report-on-mobile-money-2026

https://www.alkami.com/resources/research/reports/retail-banking-digital-sales-service-maturity-model-report

https://www.juniperresearch.com/research/fintech-payments/emerging-payments/a2a-payments-research-report/