Generative artificial intelligence (GenAI) has gone from a hyped new technology to a game-changing force in the banking industry. Today, financial institutions have moved beyond contemplating its potential to actively implementing and scaling use cases, eager to capture the immense value it promises.

This article covers 9 GenAI applications we see working across retail banks, commercial banks, and wealth management firms – from customer-facing chatbots and credit workflows to the internal tools quietly transforming banking software development and maintenance.

Key takeaways:

- Major banks have moved past the pilot stage – GenAI is now running in production across lending, compliance, fraud detection, and customer service at institutions like JPMorgan, HSBC, Lloyds, and OCBC.

- Document-heavy workflows offer the most rapid payback, with GenAI taking over tasks that consume 60-70% of analyst time in credit, KYC, and compliance functions.

- Internal tools, such as knowledge bases, coding assistants, and meeting summarization, ship faster and deliver measurable productivity gains with lower compliance overhead, making them the right starting point for most banks.

- GenAI transforms static transaction data into personalized financial insights, enabling banks to proactively suggest relevant products based on real spending behavior and life events.

- Vendor selection in banking is a compliance decision first: data residency, PCI DSS, GDPR, and the EU AI Act each impose concrete requirements on how and where GenAI can be deployed.

Practical GenAI applications in banking services

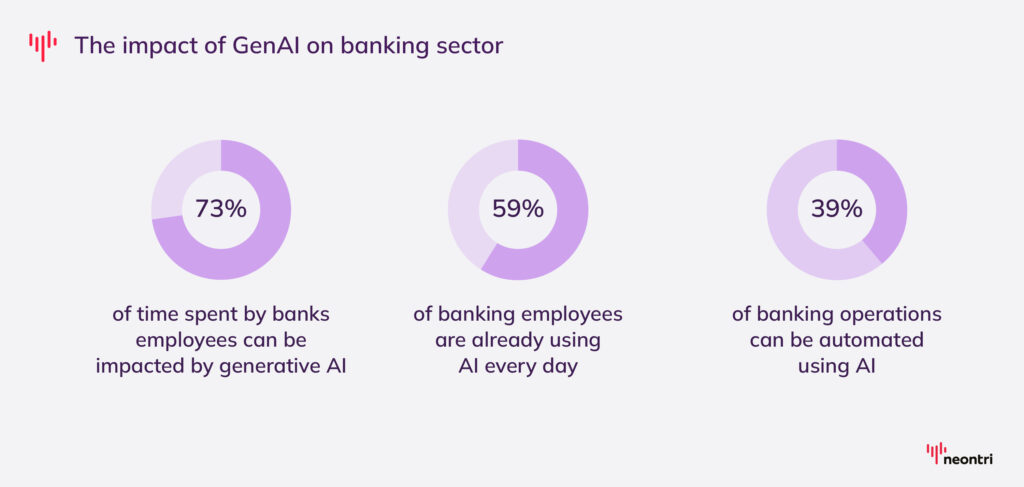

Generative AI solutions in banking have the potential to add between $200 billion and $340 billion in annual growth. Roughly three-quarters of this value is concentrated in four key areas: customer operations, marketing and sales, software engineering, and R&D.

The transformative potential of GenAI extends across the entire banking value chain, from back-office operations to how banks communicate with their customers. With these tools, banks can make data-driven decisions, catch risks before they become problems, and build new products that actually hit the mark for the people they serve.

At its core, GenAI acts like a high-powered engine for information, handling tasks that previously bogged down human teams, including:

- summarizing large volumes of information

- data classification

- performing Q&A

- sentiment analysis

- detecting suspicious behavior

- predictive modeling

- generating content.

By turning complex datasets into clear, actionable intelligence, GenAI has become an essential partner in everything from credit risk assessment to market forecasting. With that foundation in mind, let’s take a closer look at some of the most impactful use cases for GenAI in banking today.

Use case #1: Personalized investment advisor

Business problem: High-net-worth individuals receive bespoke financial advice, while retail customers are often relegated to generic robo-advisors that offer static, one-size-fits-all portfolios based on basic risk questionnaires. These automated systems fail to account for the nuances of a user’s life, such as specific career trajectories, changing local real estate markets, or personal ethical preferences.

Solution: GenAI transforms the investment experience from a static chart into a dynamic financial dialogue. By securely processing a customer’s full financial picture, including cash flow, spending habits, and external assets, GenAI acts as a 24/7 personalized advisor. It can explain complex market shifts in plain language and proactively suggest portfolio rebalancing based on real-time life events detected in the data, such as a salary increase or a new dependent.

Example: Morgan Stanley Wealth Management puts GenAI directly into the advisor-client workflow. The company used an OpenAI-powered engine to turn its massive institutional research library into a personalized co-pilot for its employees and customers.

Rather than forcing clients into rigid investment buckets, the system uses a specialized tool called Debrief that, with consent, records client meetings and synthesizes hours of conversation into actionable financial strategies. This allows the AI to capture critical life nuances, such as a client’s concern over a career transition or a shift in personal values, that would typically be missed by a standard risk questionnaire.

Once these personal insights are captured, the GenAI instantly cross-references them with the bank’s vast institutional library of 100,000+ proprietary research reports. The result is a dynamic, “Portfolio of One” that aligns with both global market shifts and the client’s individual life events.

Use case #2: Client onboarding

Business problem: Know your customer (KYC) and onboarding processes are plagued by slow, resource-intensive vetting cycles that can take up to 30-90 days. Despite ongoing digitization efforts, many banks still rely on people-heavy workflows. The manual collection of documents, verification of ultimate beneficial owners, and periodic compliance reviews consume significant operational capacity.

This internal inefficiency translates directly into a deteriorating customer experience. Research from Fenergo shows that 70% of firms lost clients in the past year due to onboarding delays, while abandonment rates average around 10% as customers grow frustrated with repetitive document requests and lengthy digital workflows.

Solution: Implementation of GenAI in the banking industry is replacing tedious, paper-heavy processes with scalable digital systems that can handle increased onboarding volumes without compromising quality or speed. By handling complex financial data with higher precision than human-led processes, AI tools minimize clerical errors, improve accuracy throughout the verification cycle, and ensure the integrity of customer data.

The following are key examples of how artificial intelligence can be applied to transform various aspects of banking services:

- Automated document processing. GenAI excels at extracting and interpreting information from various document types. It can automatically populate onboarding forms by analyzing documents submitted by clients, significantly reducing manual data entry and associated errors.

- Regulatory compliance. Generative AI can ensure that customers meet all KYC requirements by automatically flagging any missing information or potential compliance issues.

- Streamlined customer interactions. AI-powered virtual assistants can guide clients through the onboarding process by answering questions and providing explanations, reducing the likelihood of incomplete submissions.

- Real-time verification. GenAI technology can perform real-time verification of client information against various databases, detecting fraudulent behavior and enhancing security.

Example: Citigroup is actively applying AI to target approximately 50 high-frequency internal processes, including client and employee onboarding and KYC-related flows.

The technology has already helped to transform a manual, hour-long pre-account-opening document review into a 15-minute automated step for its U.S. services division. Rather than deploying a single model, the bank adopted a portfolio approach: document-processing workflows that handle OCR and NLP, automated data migration from legacy systems, and AI-assisted coding and testing tools that run in parallel.

Use case #3: Transaction categorization

Business problem: Traditional rule-based categorization systems struggle with messy merchant strings and non-standard descriptions, leading to poor customer experiences and inaccurate financial insights. For the bank, this results in high call volumes from confused customers and lower trust in digital banking tools.

Solution: AI-powered algorithms can automatically categorize financial transactions, giving customers detailed insights into their spending habits. Transaction categorization solutions gather payment data from various sources, including banks, payment processors, and financial apps, and then preprocess it, cleaning and normalizing it into a structured format. By utilizing Large Language Models (LLMs) specialized in semantic reasoning, banks can interpret fragmented transaction metadata to accurately categorize spending into hundreds of niche sub-sectors.

Example: Royal Bank of Canada’s AI-powered digital assistant, NOMI, can turn static transaction histories into a dynamic, categorized financial map by automatically sorting every debit and credit payment from linked accounts into intuitive groups like “dining” or “transport.”

This categorization layer enables a more interactive experience through the Ask NOMI interface. Customers can query their spending history using natural language, turning a list of dates and amounts into a searchable tool for day-to-day cash flow management.

Use case #4: Loan application summarization for credit officers

Business problem: A commercial loan application can include 200-500 pages of financial statements, legal documents, and business plans. This means credit officers have to sift through tons of unstructured data for each application, spending 60-70% of their analysis time on document comprehension rather than on the credit judgment.

Solution: GenAI transforms loan analysis by taking over the most time-consuming part of the process – document processing. A document ingestion pipeline parses large application packages (including PDFs, scanned files, and images using OCR where needed) and feeds them into a long-context LLM. The model extracts key signals such as financial performance, debt-to-income ratios, cash flow trends, and indicators of business stability, then synthesizes them into a clear, structured view of the applicant’s financial position.

Instead of manually reviewing hundreds of pages, credit officers receive a concise, standardized 2-page credit memo covering the business overview, financial highlights, key risk flags, and suggested follow-up questions.

Example: HSBC’s multi-year partnership with Mistral AI spans more than 600 generative AI use cases, including document intelligence. By deploying AI to rapidly summarize loan documents, financial statements, due diligence packs, and term sheets, the bank enables staff to shift their focus from manual data extraction to expert judgment and decision-making.

The system enhances this process by automatically extracting complex covenants and comparing them across multiple counterparties, providing credit committees with precise, synthesized insights for faster reviews. It also introduces multilingual reasoning and translation capabilities, allowing the bank to translate, validate, and interpret information across multiple languages, an essential feature for cross-border client interactions and globally distributed data sources.

Use case #5: Customer service chatbots

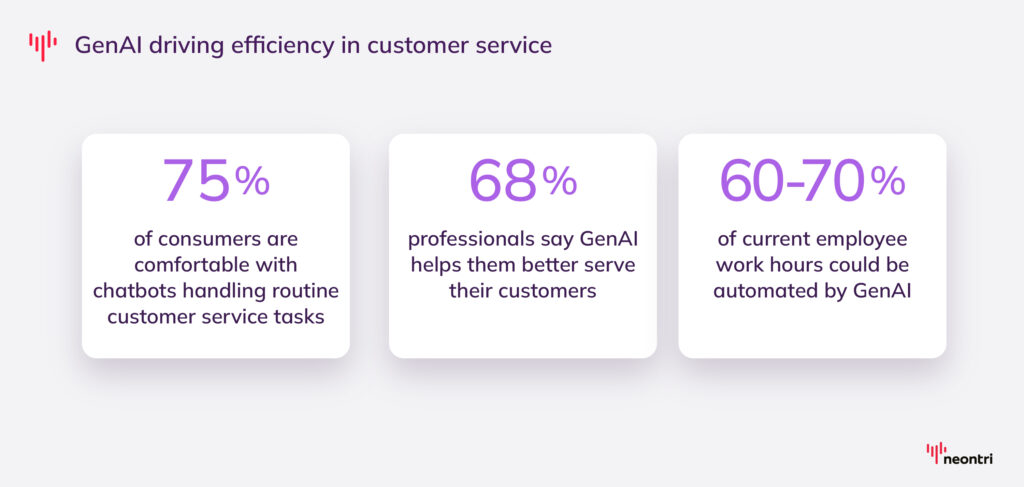

Business problem: Legacy, rule-based chatbots rely on static decision trees and can’t capture natural language nuances or intent. Without real-time access to a customer’s specific account history, these bots offer nothing but generic FAQs. This forces customers to repeat their entire story from scratch once they finally manage to escalate to a human agent, often for something as simple as questioning a fee or identifying a transaction.

On the other hand, relying exclusively on traditional customer support imposes a massive time tax on clients. During peak hours, waiting on hold for 20-45 minutes is common, support often disappears after 5 PM, and every transfer to a new agent means starting the conversation from scratch. All of this creates friction at a time when people expect their bank to respond with the same speed and continuity as any other digital service they use.

Solution: With banking clients managing accounts across multiple platforms – mobile apps, websites, ATMs, and contact centers – GenAI ensures consistent, high-quality service at every touchpoint. At the heart of this transformation are AI-powered chatbots, which serve as the front line of digital banking support. These intelligent virtual agents handle routine inquiries, such as password resets or payment tracking. However, they recognize when they’re out of their depth and automatically escalate complex issues, such as mortgage eligibility questions or loan approval status, to financial advisors.

But GenAI goes beyond automation – it brings emotional intelligence into the equation. By analyzing customer behavior, transaction patterns, and historical data, it can anticipate needs and take a proactive approach. Whether it’s reminding users of upcoming payments, flagging unusual activity, or suggesting budgeting tips, the AI responds with context and care. This seamless, personalized interaction builds customer trust and enhances the overall banking experience.

Example: J.P. Morgan Payments’ GenAI-powered virtual assistant provides clients with a 24/7 conversational interface for reporting queries. It replaced a static help system with a context-aware assistant that understands natural-language questions and responds with precise, sourced answers rather than generic documentation links.

The assistant is built on a Retrieval-Augmented Generation (RAG) framework, with LLM-as-a-judge evaluation to test correctness, completeness, and hallucinations during development. Iterative prompt refinement, retrieval tuning, and vector store expansion were used to progressively improve output accuracy before client-facing launch.

Use case #6: Regulatory compliance document analysis

Business problem: According to a CUBE survey, 82% senior compliance decision-makers track between 26 and 100 regulatory alerts each month across multiple jurisdictions, with 39% handling more than 50 change events. With officers spending the bulk of their time manually reading updates, mapping them to affected business lines, and rewriting internal policies, a single significant legislative update can take weeks just to process. This heavy operational drag explains why 74% of financial institutions take more than a year to fully implement new regulations – a prolonged exposure window during which the bank operates with elevated compliance risk.

Solution: GenAI automates the most labor-intensive part of the compliance cycle – reading, interpreting, and mapping regulatory text. When new regulations are published, an ingestion pipeline feeds them into an LLM alongside the bank’s internal policy library. The model identifies which policies are affected, flags gaps between current practice and new requirements, and drafts proposed amendments for compliance officer review. This way, humans can focus on judgment and sign-off rather than document comprehension.

Example: Deutsche Bank’s Compliance Technology team faced a growing volume of queries from bankers operating across regions, ranging from cross-border transaction guidance to nuanced regulatory interpretations. Every question required a compliance officer to manually parse dense policy documentation before responding, creating bottlenecks that slowed client-facing decisions and stretched an already pressured function.

To streamline the workflows, the bank collaborated with Tata Consultancy Services to deploy an AI-driven conversational digital assistant built on Google Cloud Platform. By leveraging GenAI alongside reinforcement learning and strict data privacy guardrails, the assistant enables staff to input complex regulatory questions in natural language and receive context-aware, sourced answers around the clock. The implementation has transformed the bank’s operational agility by slashing the response times from over 24 hours to a matter of seconds.

Use case #7: Fraud pattern detection narrative generation

Business problem: Traditional machine learning fraud models are highly effective at flagging suspicious transactions and producing probability scores, but they fail to explain why a specific event was flagged. As a result, analysts must manually piece together the narrative, digging through raw transaction logs, IP data, device fingerprints, and behavioral signals before they can confidently make a decision or escalate a case. This investigative bottleneck severely slows down the freezing of compromised accounts and makes timely reporting to regulatory authorities difficult.

Solution: GenAI adds depth to the existing fraud detection infrastructure. It analyzes the anomalies detected by the core ML model, translating them into a structured investigation summary: why the transaction was flagged, which known fraud typologies the pattern resembles, and the recommended next steps. Analysts start each case with context rather than building it from scratch, thereby reducing investigation time and improving the consistency and auditability of case documentation.

Example: Lloyds Banking Group has complemented its fraud prevention operations with new capability – AI Call Assist. Before this system was introduced, agents spent several minutes per call on manual note-taking and triage – a process that slowed investigations, created inconsistencies across records, and delayed freezing of compromised accounts. AI Call Assist eliminates this bottleneck by generating near real-time transcripts right during the fraud and dispute calls.

Once the conversation ends, the GenAI engine analyzes the dialogue, extracts key claims, actions, and outcomes, and automatically produces a structured case summary. Frontline fraud analysts can immediately review, edit, and approve the generated narrative before saving it to the customer’s case file. By replacing manual note-taking with standardized, AI-generated documentation, Lloyds has reduced average call handling times by 3% across approximately 700,000 monthly calls.

Use case #8: Internal knowledge base for branch staff

Business problem: Branch staff must keep pace with a vast and frequently updated landscape of products, interest rates, and procedural requirements, but this information is typically scattered across fragmented SharePoint sites, PDF manuals, and institutional knowledge. This forced reliance on tribal knowledge leads to inconsistent customer advice and significantly extends onboarding timelines, with new employees taking 6-12 weeks to become fully operational.

Solution: GenAI transforms branch operations by acting as an intelligent co-pilot that consolidates fragmented data into a single, conversational interface. A RAG pipeline ingests the bank’s entire repository of manuals, policy documents, and rate sheets, allowing staff to ask natural language questions and receive instant, accurate answers with direct source citations.

Example: Knowledge Central AI is a cornerstone of the Canadian Imperial Bank of Commerce’s (CIBC) internal AI ecosystem. It is purpose-built to eliminate information silos and enable contact center and client-facing teams to instantly surface product and procedural information. Developed as a RAG chatbot plugged into the bank’s core policy directories, the system helps resolve common client inquiries and reduce internal call escalations.

However, the early rollout also surfaced important technology limitations. The team found that not all enterprise data was suitable for model consumption due to formatting inconsistencies and other structural issues, which required reducing the initial content scope to a more manageable dataset for the pilot phase. In addition, certain LLMs struggled to deliver specific responses with 100% accuracy, leading to a deliberate narrowing of use cases involving strict verbatim instructions. By matching data readiness directly to the model’s strengths, the bank achieved high team engagement and a continuously improving system that allows staff to focus less on searching and more on deepening client relationships.

Use case #9: Code generation for core banking system maintenance

Business problem: Maintaining legacy core banking systems is a massive operational burden because they rely on decades-old codebases written in languages like COBOL or specialized PL/I. As veteran developers retire, institutions face a severe talent shortage, leaving remaining teams to spend up to 80% of their time reverse-engineering undocumented code just to implement routine updates or fix bugs. This knowledge gap severely delays feature deployments and increases the risk of catastrophic system downtime during manual maintenance cycles.

Solution: GenAI accelerates digital banking modernization through specialized LLMs trained on mainframes and financial code repositories. Such models analyze monolithic code segments and automatically generate line-by-line documentation, business logic maps, and risk assessments for proposed changes. Furthermore, they can act as an expert pair-programmer, producing syntactically accurate updates, automatically writing unit tests for edge cases, and safely translating legacy functions into modern languages like Java or Python.

Example: Oversea-Chinese Banking Corporation (OCBC) developed its own in-house generative AI coding assistant, OCBC Wingman. Deployed within a highly secure sandbox environment to protect the bank’s proprietary IP, the bot tracks developers’ active workflows, allowing them to auto-generate code, debug logic errors, and safely optimize existing systems.

In its first year, Wingman processed roughly 30,000 requests per day, delivering the output equivalent of 150 to 200 additional IT specialists. By automating routine coding and development tasks, the tool successfully drove a 20% boost in productivity and overall software engineering efficiency across the organization.

Vendor selection matrix: Matching infrastructure reality to use case requirements

By 2026, most major providers can handle heavy enterprise workloads. So choosing the right GenAI vendor is less about model quality in isolation and more about finding the best fit for the organization’s specific reality. For banks, picking a partner is a balancing act between their compliance posture, existing tech stack, and how fast they actually need to deliver value.

To help you navigate the solution landscape, the matrix below maps each provider’s strengths across the variables that matter most: best-fit use cases, indicative pricing, banking compliance certifications, and realistic time to production.

| Vendor | Best for | Typical cost | Banking compliance | Time to production |

|---|---|---|---|---|

| OpenAI (direct) | Prototyping, non-sensitive tasks | $0.01-0.06 per 1K tokens | Limited (data may leave controlled infrastructure) | 2-4 weeks |

| Anthropic (direct) | Complex reasoning and analysis | $0.003-0.075 per 1K tokens | SOC 2, HIPAA-ready | 2-4 weeks |

| Azure OpenAI | Compliance-heavy workloads | Marked up ~20% | GDPR, HIPAA, PCI DSS | 4-8 weeks |

| AWS Bedrock | AWS-native environments | Variable | SOC, GDPR, PCI | 4-8 weeks |

| Google Vertex AI | Google Cloud-native stacks | Variable | SOC, GDPR, PCI | 4-8 weeks |

| Self-hosted | Maximum data sovereignty | Infrastructure costs only | Full control | 8-16 weeks |

To balance speed and security, most banks adopt a three-tiered strategy for their GenAI infrastructure. Here is how that usually looks in practice:

- For any project touching core banking data or customer PII (Personally Identifiable Information), banks lean on platforms like Azure OpenAI or AWS Bedrock. These are the go-to because they come pre-packaged with the enterprise-grade security and compliance guardrails that legal and IT teams already trust.

- For internal tools, developer productivity aids, or quick-turnaround prototyping where data sensitivity is low, teams often use direct API access to providers like OpenAI or Anthropic.

- For use cases where data cannot leave the bank’s infrastructure under any circumstances, such as trading algorithms, M&A advisory, or proprietary risk models, banks host open-source models, like Llama or Mistral, entirely within their own private, secure environments.

The compliance layer: What every banking GenAI deployment must address

Generic AI compliance advice tells banks to “consider data privacy” and “ensure human oversight.” That’s not enough. Banking operates under some of the most specific regulatory frameworks in any industry – and several of them have direct, concrete implications for how GenAI systems must be architected, deployed, and documented.

Payment Card Industry Data Security Standard (PCI DSS)

Generative AI pipelines must be strictly isolated from the Cardholder Data Environment (CDE). Under PCI DSS 4.0, if an LLM processes any sensitive authentication data, such as full card numbers, CVVs, or PINs, the entire AI infrastructure may be subjected for a PCI audit.

To avoid this, banks must adopt a zero-card-data design principle for GenAI. This includes data tokenization and automated PII scrubbing before any model interaction, as well as enforcing policies that prevent sensitive fields from entering prompts or training datasets.

General Data Protection Regulation (GDPR)

The regulatory impact of GDPR on GenAI for banking is currently unfolding across four critical dimensions that dictate how customer data is utilized and protected:

- Purpose limitation. Data harvested for essential functions, such as fraud detection, is legally siloed and cannot be repurposed for use cases without a new lawful basis.

- Human oversight. Any decisions that carry a significant effect on individuals, such as credit denials or account freezes, cannot be fully automated. Banks must maintain a human-in-the-loop to review AI-generated resolutions and, upon request, provide customers with a clear explanation of the underlying logic behind AI processing.

- Data subject rights. Customers have the right to access, correct, or request their personal information to be deleted. This creates a technical requirement for banks to ensure that data is not embedded in model outputs or logs. In practice, this means organizations must deploy architectures that allow individuals’ data to be traced, modified, or removed on demand from AI-accessible datasets without compromising the system’s integrity.

- Data residency and cross-border transfers. If a GenAI provider processes data outside the EU, banks must ensure appropriate safeguards are in place. This is why many deployments rely on EU-hosted environments on platforms such as Microsoft Azure or Amazon Web Services to keep data within regulated jurisdictions.

EU AI Act

The EU AI Act classifies several critical banking AI applications, such as credit scoring and risk assessment, as “high-risk.” This designation mandates that financial institutions implement rigorous governance frameworks, including comprehensive technical documentation, an audit trail, and mandatory human oversight to mitigate bias and ensure fairness.

Moreover, the black box nature of generative models is legally insufficient. Banks must implement Explainability (XAI), which grants customers the right to an explanation of an automated decision. For example, if an AI denies a loan, the system must be able to provide a human-readable justification that identifies specific factors, such as debt-to-income ratios or payment history, to ensure the institution meets its legal burden of transparency and non-discrimination.

We don’t just follow trends – we help banks lead with GenAI

Want to see GenAI in action?

Neontri: Harnessing the power of GenAI for banking innovation

At Neontri, we understand the unique challenges faced by the financial sector. We seamlessly implement GenAI into solutions we develop for our clients, consistently pushing the boundaries of what’s possible within existing banking systems.

A great example of this is a recent project where we built a multi-tenant SaaS platform for a fintech partner. It serves as a blueprint for how artificial intelligence should be introduced into regulated environments. At the heart of the platform sits an AI-powered decisioning engine that automates complex scoring and credit workflow decisions for loan and credit providers.

The challenge wasn’t just technical.

The challenge here went well beyond the code. We needed to create a cloud-native platform that was fully compliant with PSD2 and GDPR, integrated with third-party risk assessment services, and remained accessible for non-technical users via a low-code/no-code interface.

Our team took full ownership of the architecture design and the entire product development lifecycle. The result is a scalable, security-first platform that has since been adopted by four end clients and serves as the foundation for our partner’s international expansion.

Final thoughts

The future of banking and financial sectors is undoubtedly intertwined with the advancement of GenAI. By automating routine tasks and facilitating data-driven decisions, this technology allows banks to focus more on improving customer satisfaction and developing innovative financial services.

FAQ

Which banking use cases have the highest ROI?

The highest ROI in banking comes from AI-driven fraud detection and automated credit risk assessment, which provide immediate value by preventing capital loss and expanding the lending pool. GenAI for customer service is another strong performer, reducing cost per interaction by 30-50% and automating up to 60-70% of routine inquiries, including complex back-office workflows such as dispute handling and onboarding. Hyper-personalized product recommendations also drive significant returns by lifting conversion rates by 5-15% alongside operational savings.

When should a bank build vs buy its own GenAI pipeline?

Banks should buy off-the-shelf GenAI pipelines for standard productivity tasks, such as document summarization and basic customer service. Vendors like Microsoft Copilot or Salesforce Einstein cover these adequately, go live in weeks, and carry pre-negotiated compliance certifications.

For core strategic functions, such as proprietary credit scoring or high-frequency trading, where data sovereignty, competitive differentiation, and strict regulatory compliance are paramount, it is better to take the build route.

How do banks handle hallucinations in customer-facing GenAI?

Banks mitigate GenAI hallucinations by implementing Retrieval-Augmented Generation (RAG), which draws AI responses from the bank’s verified databases rather than relying solely on the model’s training data. They also use human-in-the-loop workflows and strict guardrail software that scans outputs for compliance and accuracy before they reach the customer.

What’s the difference between GenAI and traditional AI in banking?

Traditional AI in banking is predictive and analytical. It excels at structured tasks, typically those that require classifying inputs into categories or producing numerical scores. In contrast, Generative AI is creative, capable of producing text, summaries, code, and structured outputs from unstructured inputs. While traditional AI identifies “what” is happening, GenAI explains “why” or “how” in human-readable terms.

Another distinction is the interface. Traditional AI runs silently in the background within the pre-set parameters. GenAI interacts with humans in natural language, handling novel inputs it wasn’t explicitly trained on.

How do banks measure GenAI ROI?

Banks measure GenAI ROI using a three-tier framework that tracks:

- revenue lift from hyper-personalized marketing offers, cross-selling opportunities, customer retention improvement, or accelerated loan disbursement timelines that capture market share from slower competitors

- immediate efficiency gains, calculated by multiplying hours saved per week × fully-loaded staff cost × number of users

- cost-per-transaction, which compares manual processing costs vs. AI-assisted costs per unit, for example, KYC documents processed, loan applications reviewed, and support tickets resolved.

References

- https://www.retailbankerinternational.com/news/canadas-major-banks-optimise-ai-to-drive-growth-enhance-customer-experience/

- https://resources.fenergo.com/newsroom/global-financial-institutions-struggle-with-rising-client-losses-and-compliance-costs-as-ai-adoption-increases-fenergo

- https://asper.app/rbc-budget-app-features-nomi-asper-alternative-2025-asper/

- https://developer.payments.jpmorgan.com/blog/product/virtual-assistant-ai-reporting

- https://www.gend.co/blog/hsbc-mistral-ai-partnership

- https://www.fstech.co.uk/fst/HSBC_Partners_With_Mistral_AI_To_Boost_GenAI_Adoption.php

- https://www.morganstanley.com/press-releases/ai-at-morgan-stanley-debrief-launch

- https://letsdatascience.com/news/citi-uses-ai-to-speed-account-openings-eaace5d4

- https://www.tcs.com/what-we-do/industries/banking/testimonial/deutsche-bank-accelerates-compliance-ai-digital-assistant

- https://medium.com/ai-at-lloyds-banking-group/outsmarting-fraudsters-with-ai-call-assist-lloyds-banking-groups-intelligent-agent-for-customer-c62d2307f22b

- https://www.techinasia.com/ocbc-developed-aipowered-wingman

- https://www.mckinsey.com/capabilities/tech-and-ai/our-insights/the-economic-potential-of-generative-ai-the-next-productivity-frontier